The fallout from the global spread of Covid-19 has already produced cascading sudden economic stops that disrupted markets in record speed, triggering negative feed-back loops and requiring unprecedented policy support. In response to the economic shock and the potential damage to both corporations and households, policymakers of all major economies launched massive packages of monetary and fiscal stimulus, increasing the overall level of indebtedness in their countries.

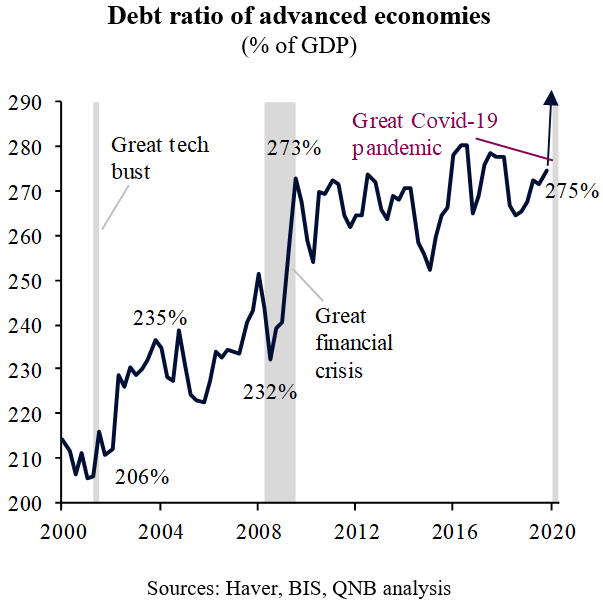

If history is any guide, periods following recessions or acute financial stress often trigger rapid spikes in debt ratios. This tends to be a result of GDP contraction and demands for liquidity support and supplemental fiscal spending, which requires additional borrowing from all sectors, especially governments and corporates. In the early 2000s, the burst of the global tech bubble triggered a short recession that led to a significant increase of debt ratios in advanced economies, from 206% of GDP to 235%. Similarly, after the great financial crisis of 2008-09, debt ratios in advanced economies skyrocketed from 232% to 273% of GDP in a short period of time.

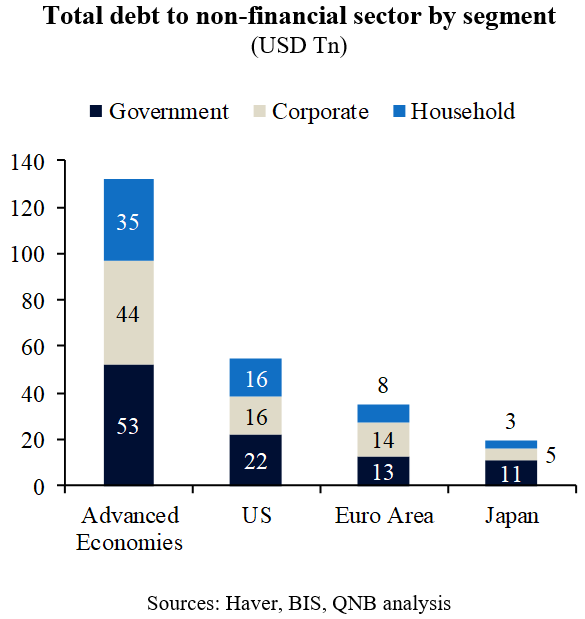

According to the Bank for International Settlements (BIS), total credit to the non-financial sector (households, corporates and governments) of advanced economies amounted to USD 132 trillion (Tn) by the end of 2019, representing 275% of their gross domestic product (GDP). The total amount included USD 35 Tn of debt to households, USD 44 Tn to non-financial corporates and USD 53 Tn to governments. The US, the Euro area and Japan concentrate a large share of the total debt of advanced economies. This includes USD 54 Tn or 254% of GDP for the US, USD 35 Tn or 262% of GDP for the Euro area and USD 19 Tn or a staggering 381% of GDP for Japan.

Such debt levels and ratios have been increasing rapidly in recent months and are expected to increase substantially over the short-term. This will be driven by high credit demand from governments and corporates. A massive increase in budget deficits (more than 10% of GDP in most of the advanced economies) would normally produce large spikes in bond yields and credit contraction to the private sector, tightening financial conditions. This would be detrimental to the highly leveraged corporate and government sector, as it would increase the overall debt burden. Thus, additional debt has been partially funded (directly or indirectly) by central banks, in an attempt to hold interest rates down even during a fiscal expansion.

While we believe that the current crisis indeed requires extraordinary policy support, we recognize that both the malaise (Covid-19 shock) and the cure (policy support) will accelerate existing imbalances of major economies, particularly debt issues in the US, the Euro area and Japan. Debt levels were already elevated in these countries before the pandemic, and expansionary monetary and fiscal policies are creating an additional increase of overall indebtedness.

With interest rates now at or close to zero in all three major advanced economies, and with debt ratios reaching all-time highs, monetary policy cannot be “normalized” until debt ratios improve. Moving forward, given the levels of government and corporate indebtedness, central banks will not be able to respond to the business cycle as they are used to. If the recession deepens or a new recession unfolds, there is no policy room for additional support without heavy coordination with fiscal authorities. If a recovery ensues and the economy overheats, there would be no room for rate hikes to contain inflation without severe negative effects on the balance sheets of corporates, households and sovereigns. As debt levels grow, higher interest rates generate ever more pressure on debtors, due to the increase in costs to roll over or service existing debt.

All in all, the debt situation of advanced economies is elevated. High and rising indebtedness is expected to produce challenging conditions in the near future. However, the problem is not unsolvable. Appropriate responses will require sensible policy measures such as austerity, debt restructuring and re-distribution. Our view is that such measures are necessary to prevent disruptive outcomes for creditors and debtors alike. Inadequate policy responses would be rather detrimental for the majority of households, corporates and governments.

Download the PDF version of this weekly commentary in English or عربي