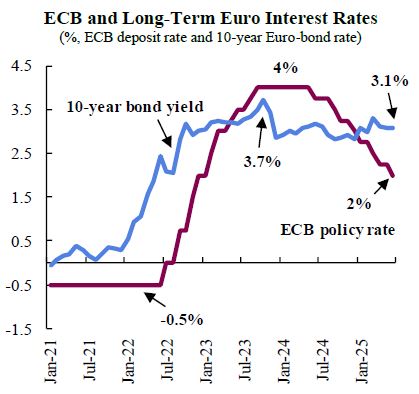

Spiralling inflation in the Euro Area was finally stabilized last year after an unprecedented cycle of policy rate increases by the European Central Bank (ECB). The most aggressive tightening sequence in the history of the ECB took the benchmark interest rate to 4%, as a response to the unprecedented post-Covid inflationary shock. This was followed by a “holding” period of nine months, as the central bank waited for inflation to shorten the gap between the peak of almost 11% and the 2% target of monetary policy.

Interest rate cuts finally began in June last year at a cautious pace, as ECB officials gained confidence in diminishing price pressures. This brought the deposit rate to 2%, a level broadly within the “neutral range” that implies that monetary policy is neither expansionary nor contractionary. With inflation recently oscillating narrowly around the 2% mark, the ECB must now calibrate the appropriate terminal rate.

In our view, the macroeconomic outlook warrants two additional rate cuts this year. In this article, we discuss three key factors behind our analysis.

First, there is an increasing likelihood that inflation will meaningfully undershoot the 2% target of the ECB. The latest release of consumer prices displayed a headline inflation rate of 1.9% in May, before hitting the 2% target in June. Additionally, reduced wage increases will further diminish price pressures in the labour-intensive services sector, which typically exhibits highly persistent inflation.

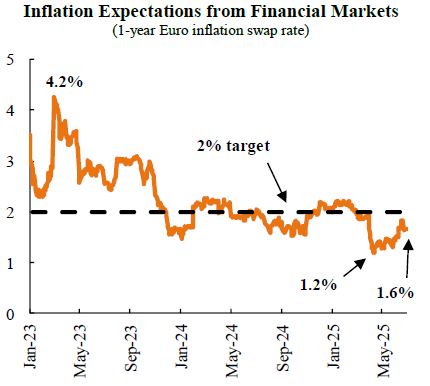

More importantly, markets are signalling that inflation will decrease in the year ahead. Financial instruments can provide useful information regarding the expected evolution of macroeconomic variables. Specifically, the euro-inflation swap-rate reveals inflation expectations of investors. Since the peak of 4.2% reached early 2023, market inflation expectations have been on a downward, even if irregular, trend. For the last four months, expectations for a year ahead have remained below the 2% target, after reaching a low of 1.2%. The disinflation expectations add to concerns that the ECB will undershoot its target, giving room for additional interest rate cuts.

Second, after lingering on the verge of a recession for the last two years, the Euro Area is set for another period of underwhelming growth performance. The recent prints of the Purchasing Managers Index (PMI) point to a stagnant economic outlook. The PMI is a survey-based indicator that provides a measurement of improvement or deterioration in the economic outlook. The composite PMI, which tracks the joint evolution of the services and manufacturing sectors, has remained below or close to the 50-point threshold that separates contraction and expansion since August last year. The conditions for the manufacturing sector are particularly negative, with the PMI for industry having stayed in the contraction range for the last three years, amid the region’s energy crisis, geopolitical uncertainty, and escalating global trade conflicts. In this context, analysts’ consensus expectations, as well as the ECB staff, forecast 0.9% growth of real GDP this year. Given the weak economic outlook for the Euro Area, some of the members of the ECB’s Governing Council have made the case for additional monetary stimulus.

Third, credit growth in the Euro Area remains lacklustre. In spite of the significant interest rate cutting cycle implemented by the ECB, long-term interest rates have not shown a major reduction. The 10-year euro-bond rate remains above 3%, and largely unmoved in the last two years. Long-term interest rates are key for the economy, given their influence on business investment and household demand. Additionally, the ECB continues to revert the balance sheet expansion that was put in place during the pandemic, a normalization that is restraining the availability of credit. As a result of lower liquidity and higher credit costs, volumes of credit to firms are still contracting in real terms, restraining investment and signalling to the ECB the need for lower interest rates.

All in all, in spite of erratic short-term price pressures and tariff-wars alarms, we believe the balance of risks continues to lean more heavily on weak growth performance over inflation concerns. With this outlook, the ECB could implement two additional 25 b.p. cuts this year, taking the deposit interest rate to 1.5%.

Download the PDF version of this weekly commentary in

English

or

عربي