In recent decades, Indonesia has stood out for its exceptional performance in terms of economic growth and stability. During 2000-2024, the Indonesian economy expanded at an average growth rate of 5%. This is a remarkable track record for the fourth most populous country in the world, weathered during a testing period that included the challenging years of the Global Financial Crisis and the Covid-pandemic.

At the end of last year, a deceleration in economic activity began to take place, amid post-presidential election uncertainty, softening commodity prices, and a hawkish stance of monetary policy. This year, President Trump’s “Liberation Day” established sweeping tariffs upon its trade partners across the world, threatening major disruptions in the global economy. The US imposed a 32% tariff on Indonesian goods, which represents a meaningful threat to its export sector. The tariffs were then put under “pause,” as the Southeast Asian nation works on an agreement that includes preferential tariffs on US goods, increased access to its critical minerals, and larger US fuel imports.

The Indonesia Activity Tracker (IAT) is a timely barometer that can gauge the momentum in the Indonesian economy, summarizing information from key high-frequency activity indicators. After the 5.3% year-over-year growth peak reached in October, the growth pace began to moderate, until it stabilized at the long term average growth rate of 5%.

Despite this apparent stabilization, significant uncertainty remains at the global stage. In our view, despite considerable headwinds, the macroeconomic outlook remains positive for Indonesia. In this article, we discuss the three main factors that support our outlook.

First, consumption will remain a robust driver of growth for this year. Consumption represents 55% of the Indonesian economy and is therefore a major factor that determines the country’s growth performance. The strength in consumption is sustained by a resilient labour market, which has shown a remarkable recovery since the Covid-pandemic. The unemployment rate has fallen from a peak of 7.1% in 2020, to 4.8% according to the latest print of 2025, reaching the lowest mark since 1998. Adding support to household spending, in recent months the Indonesian government has announced a battery of stimulus measures, including sizable electricity discounts for 79 million households, food assistance for 18.3 million low income-families, and cash-transfers for low-income workers. Resilient labour markets, together with stimulative government policies will provide ample backing to consumption this year.

Second, controlled inflation and the stabilization of the rupiah (IDR) have created room for Bank Indonesia to implement expansionary monetary measures. The annual inflation rate has remained comfortably subdued this year, close to the lower bound of 1.5-3.5% target range of monetary policy. Additionally, the IDR has regained stability, appreciating by close to 3.5% since its historic low on April 9. Low inflation and a more stable IDR allowed Bank Indonesia to cut its policy rate by 25 basis points (b.p.) in May to 5.5%, the third rate cut since September last year. Additionally, the central bank has implemented a series of measures to boost credit in the economy including the reduction of reserve requirements, the increase of limits on foreign-source funding for local banks, the pledge to purchase USD 9.3 Bn in government bonds in the secondary market, and committing USD 7.9 Bn in funding for the state’s affordable housing program, among others. Thus, monetary conditions are set to stimulate economic momentum.

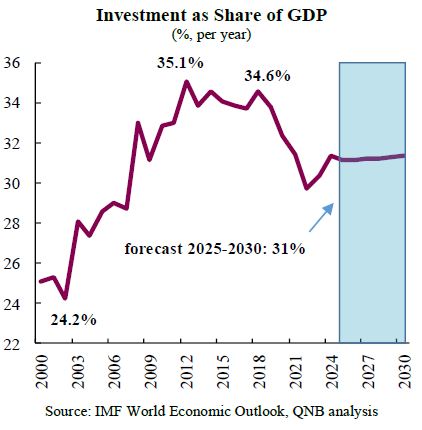

Third, Indonesia continues to develop a robust pipeline of large-scale infrastructure and CAPEX projects that will underpin investment flows and add to production capacity. Infrastructure investment is expected to remain one of the main priorities of the new administration. Major projects are developing in sectors such as transportation (roads, railways, airports, and ports), energy (including renewable energy and a major refinery), and facilities needed for the operation of new manufacturing plants. Additionally, the newly launched sovereign wealth fund Danantara has received the mandate to target projects in natural resources processing and artificial intelligence development. Public investment will add a boost to sustain a healthy level of aggregate investment, which will remain above 30% of GDP and contribute to a firm pace of economic growth.

All in all, although significant headwinds should result in a non-negligible deceleration of economic growth, Indonesian macroeconomic fundamentals remain robust on the back of resilient consumption, monetary policy stimulus, and a strong pipeline of infrastructure and Capex projects.

Download the PDF version of this weekly commentary in

English

or

عربي