The global economy is now well into its recovery from the sharp falls in activity related to the initial impact of Covid-19. However, there is considerable variety across countries and regions of the world. Indeed, it should be no surprise that government policy is instrumental in determining the size, shape and speed of recovery.

Here we use a simple framework based on the split of activity between manufacturing and services, specifically using the Purchasing Manager Index (PMI). We then apply our framework to the recovery and outlook for three key countries/regions of the world (China, Euro area and US), using it to review the impact of various forms of policy support on the shape of the economy in each country or region.

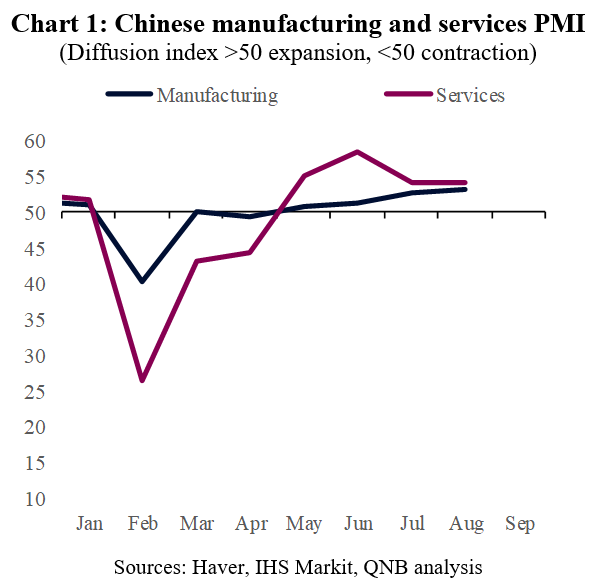

China responded to Covid-19 with aggressive lockdown measures that were effective in getting the virus under control domestically, but were unable to prevent the virus spreading abroad. The lockdowns lead to a sharp slowing in economic activity that peaked in February (Chart 1). Chinese policymakers responded with significant fiscal and monetary stimulus. The speed and power of the policy response limited the fall in manufacturing activity, in particular. This is because Chinese policy stimulus, focuses on using fiscal and monetary policy to encourage firms and local governments to invest infrastructure and real estate projects. This investments boost demand for raw materials (such as glass and steel) and the supply chains that produce them, thus supporting employment and the income. Indeed, the Chinese economy has recovered more strongly than we initially expected and returned to growth by the end of Q2 2020.

China responded to Covid-19 with aggressive lockdown measures that were effective in getting the virus under control domestically, but were unable to prevent the virus spreading abroad. The lockdowns lead to a sharp slowing in economic activity that peaked in February (Chart 1). Chinese policymakers responded with significant fiscal and monetary stimulus. The speed and power of the policy response limited the fall in manufacturing activity, in particular. This is because Chinese policy stimulus, focuses on using fiscal and monetary policy to encourage firms and local governments to invest infrastructure and real estate projects. This investments boost demand for raw materials (such as glass and steel) and the supply chains that produce them, thus supporting employment and the income. Indeed, the Chinese economy has recovered more strongly than we initially expected and returned to growth by the end of Q2 2020.

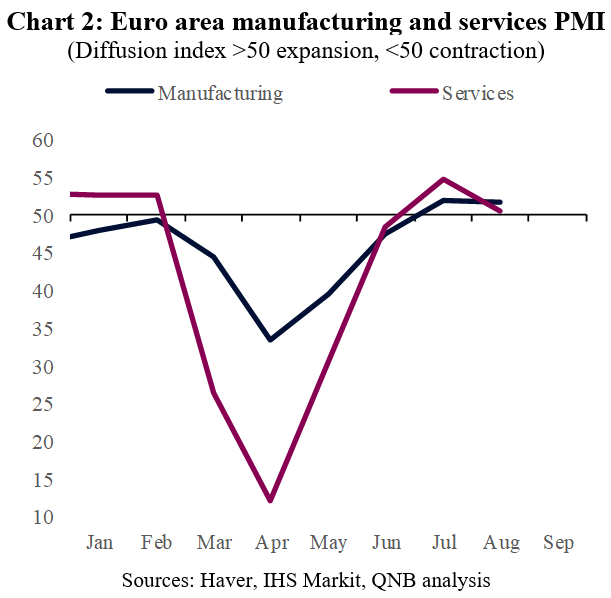

Covid-19 next hit Europe, where elderly populations, allowed the virus to have a greater impact. European policy-makers were caught off-guard, before they also responded with aggressive lockdown and social distancing measures. This in-turn lead to a peak slowing of economic activity April (Chart 2). Europe has responded to the crisis in three main ways. First, the ECB has further loosened monetary policy via lower interest rates and additional asset purchases, also called quantitative easing (QE). The second aspect of the European policy response to Covid-19 is a focus on employment support programs that subsidises the retention of workers by firms as an alternative to making them unemployed. This obviously helps to support employment and incomes and led to a stronger rebound in services. Third, and most important, conservative “core” countries have agreed to the issuance of mutual debt to help fund the policy response to Covid-19. This is of particular benefit to countries like Italy and Spain, which have much less fiscal space themselves. This is one of the factors that leads us to expect outperformance from the Euro area economy in the second half of the year.

Covid-19 next hit Europe, where elderly populations, allowed the virus to have a greater impact. European policy-makers were caught off-guard, before they also responded with aggressive lockdown and social distancing measures. This in-turn lead to a peak slowing of economic activity April (Chart 2). Europe has responded to the crisis in three main ways. First, the ECB has further loosened monetary policy via lower interest rates and additional asset purchases, also called quantitative easing (QE). The second aspect of the European policy response to Covid-19 is a focus on employment support programs that subsidises the retention of workers by firms as an alternative to making them unemployed. This obviously helps to support employment and incomes and led to a stronger rebound in services. Third, and most important, conservative “core” countries have agreed to the issuance of mutual debt to help fund the policy response to Covid-19. This is of particular benefit to countries like Italy and Spain, which have much less fiscal space themselves. This is one of the factors that leads us to expect outperformance from the Euro area economy in the second half of the year.

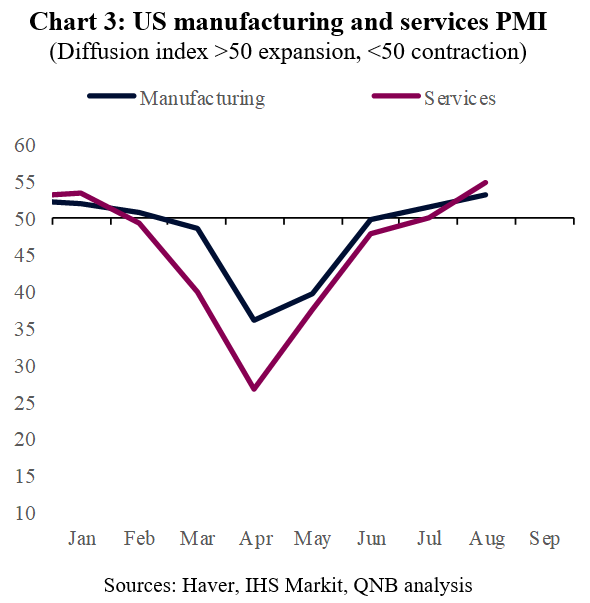

Finally, we turn to the US, where an initial lack of testing masked the true spread of Covid-19. The result was a delayed, but larger and more prolonged surge in cases. The initial impact on economic activity was more moderate than in the Euro area, but still peaked in April (Chart 3). However, the recovery has been more gradual and moderate than in China or Europe. The US policy response has two main elements. First, the US central bank (the Fed) “threw the kitchen sink at the problem” (See: US Fed fully invested in mega-intervention to support the economy), with QE infinity and a range of other tools, going well beyond the firepower deployed during the GFC. Second, the fiscal response has become bogged down by partisan politics in the run-up to November’s presidential election (See: Further USD 1.5-2 Trillion of US fiscal stimulus delayed but still likely). The uncertainty around the persistence of income support measures for laid-off workers is a particular headwind for the services sector. We therefore remain cautious about the strength and speed of the US recovery.

The over-arching point we draw from our analysis is that government policy is instrumental in determining the true speed, strength and shape of the recovery. Chinese policymakers have doubled down on stimulating the economy via infrastructure investment. Europe stands out for policies to encourage firms to retain employees, which can help to preserve human capital and has social benefits, but is expensive, so cannot be maintained for long without threatening debt sustainability. The response of Fed stands out in the US, pushing many financial markets to record highs.

The policy response from the world’s largest economies has helped prevent Covid-19 from causing an even worse economic and financial crisis. However, the hit to investment, income and productivity are likely to be persistent and both fiscal and monetary stimulus cannot be maintained forever. So, after a strong bounce-back in 2021, global growth is likely to be subdued for a number of years.

Download the PDF version of this weekly commentary in English or عربي