Chinese consumer spending slowed significantly in Q2 this year, after a strong start in early 2025. In recent months, growth in real terms dropped to the lowest rate since the start of the year. Importantly, despite new incentive measures to stimulate consumption, household savings rate has been stable, pointing to the difficulty of changing entrenched household habits.

In fact, Chinese households have long been viewed as the missing piece in the country’s economic puzzle and something that goes beyond cyclical patterns. Despite government stated efforts to enact a transition from investment-led growth into services and consumption, analysts and policymakers have pointed to persistently low consumption as a drag on growth – especially in a country of 1.4 billion people with rising income levels.

This perceived underperformance is not fully without cause, as Chinese consumers have remained cautious amid waves of economic disruption: the pandemic, a prolonged property market correction, and increased policy unpredictability.

However, despite those facts, we do believe there is a general misunderstanding about the overall magnitude and importance of Chinese private consumption.

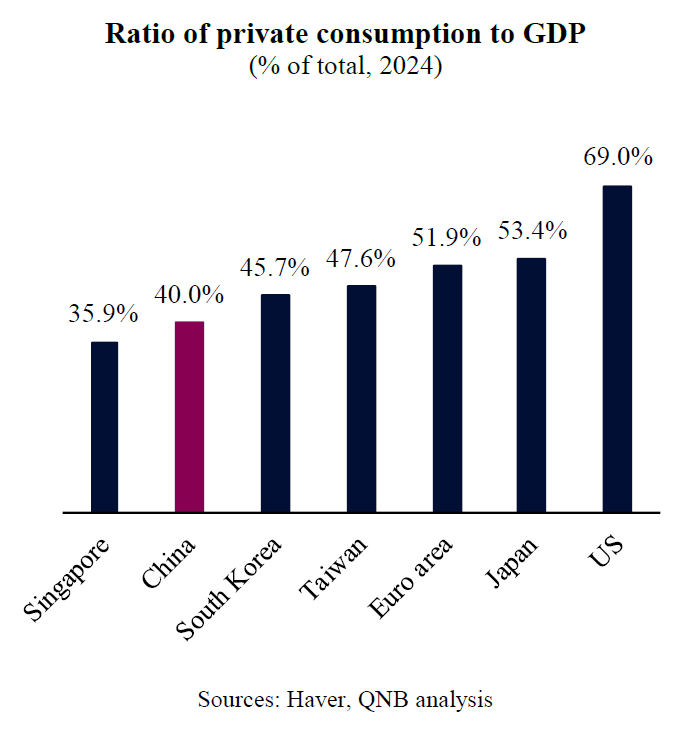

While the ratio of Chinese consumption over headline GDP cannot be compared to those found in affluent, highly consumerist, private sector driven economies, such as the US, it does not deviate significantly from the ratio from other advanced economies. This is particularly the case for advanced manufacturing, export-oriented economies from Asia, such as Japan, South Korea, Taiwan, and Singapore – countries that adopt an economic model that China emulates.

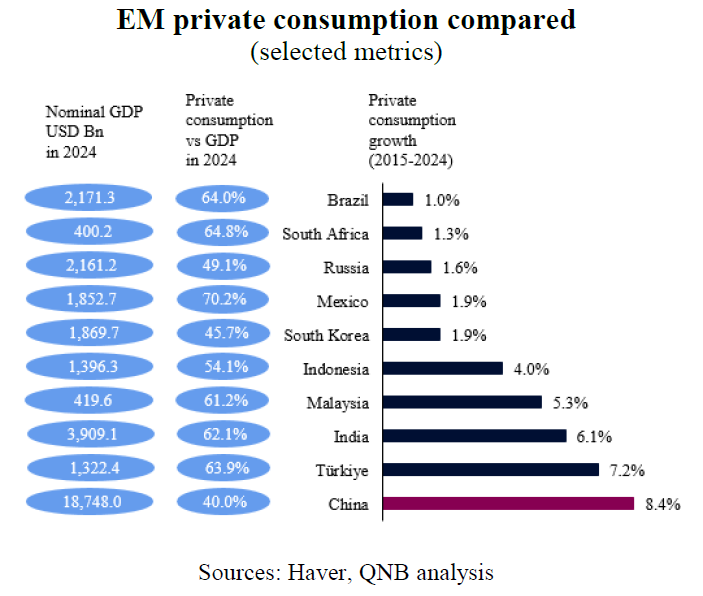

Moreover, in terms of growth dynamics, Chinese consumers have comfortably outperformed their peers even in the most growth-prone large emerging economies of the BRICS (Brazil, Russia, India, China, and South Africa) and MIST (Mexico, Indonesia, South Korea, and Türkiye) over the last decade.

In addition to those more constructive facts on Chinese household consumption, we believe that the next phase of the country’s growth story could see consumers playing a much more central role. Not only are there strong structural reasons for this shift, but recent policy direction and macro data also support an even more positive outlook. In particular, we highlight three main arguments.

First, according to the People’s Bank of China (PBoC), the local central bank, personal deposits in the Chinese banking system increased from USD 11.8 trillion pre-pandemic to USD 22.3 trillion in May 2025. This impressive build-up of private savings can be quickly mobilized for more consumption or investments over the medium-term, if confidence in the future is further restored. This would contribute for continued consumer growth and an increase in the overall share of private consumption on GDP. However, the bar is high for a significant increase of consumer spending in China. Households in China tend to be conservative with their finances and prefer to save more on the back of limited social support system from the government. Despite this, only a small change in the savings rate would be enough to create a significant impact on consumption and investment. This is expected to take place as plans to broaden the incipient welfare system are gradually executed.

Second, China is actively aiming to further rebalance its growth model away from the need for large infrastructure investments. While much of the recent focus has been on accelerating advanced manufacturing – particularly in sectors such as electric vehicles, batteries, and semiconductors –, policymakers are equally explicit about the need to boost household demand. Beijing has outlined plans to raise the share of consumption in GDP from the current 40% to 50% by 2035. This ambition is being supported by social policy reforms, housing support programmes, lower-tier city revitalization, and support for household credit, particularly in consumer finance. Rather than temporary stimulus, this reflects a longer-term policy objective – one that aims to stabilize growth through a more sustainable, internally-driven engine of demand.

Third, structural reforms are likely to gradually reshape household risk perceptions in China. The country’s targeted real estate reforms – mortgage controls and developer deleveraging – are healing distortions in the market. While this process has temporarily dampened activity, it is gradually restoring balance to household finances, reducing systemic risk and clearing the way for more stable, confidence-driven consumption ahead. At the same time, social safety nets are expanding: pensions are being scaled up, healthcare access broadened, and unemployment insurance slowly strengthened. Taken together, these reforms reduce the perceived need for excessive precautionary savings, thereby loosening household consumption behaviour.

All in all, the Chinese consumer is a much bigger driver for growth than the consensus narrative implies. Moreover, private consumption is expected to continue to grow further on the back of a large pool of accumulated savings, an explicit policy shift toward consumption, and underlying reforms that reduce household economic uncertainty

Download the PDF version of this weekly commentary in English or عربي