The six largest countries of the Association of Southeast Asian Nations (ASEAN-6), which includes Indonesia, Thailand, Singapore, Malaysia, Vietnam, and the Philippines, have been among the fastest growing economies in the world in recent decades. A large part of these success stories is attributed to their integration to global markets through international trade. Hence, anything that threatens or engenders disruption to their trade flows can have a significant impact on their macroeconomic performance.

Since Donald J. Trump’s inauguration as president of the U.S. in January this year, escalating trade wars have taken center stage in the global media spotlight. Trump’s mercantilist view promotes national self-sufficiency and considers imports as a drain on national wealth, rather than as a factor that supports healthy economic dynamism. Thus, countries with large and persistent bilateral trade surpluses against the U.S. are more likely to become prime targets for tariffs.

The initial trade rifts began with direct threats by the U.S. of 25% tariffs on Canada and Mexico, as well as 10% tariffs on China. This was followed by warnings of “universal” and “reciprocal” tariffs against all countries and products, and targeted tariffs on all imports of steel and aluminium. In turn, other nations are evaluating their own responses, further increasing the threat of protectionism and trade wars.

In our view, however, despite a challenging global trade environment, the ASEAN-6 countries stand on firm footing to weather the storm. In this article, we discuss three key elements that support our assessment.

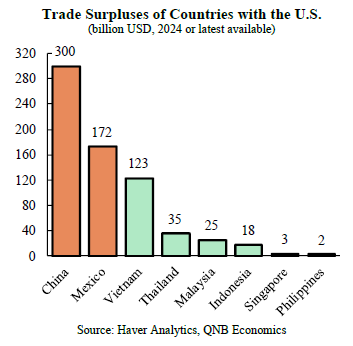

First, it is unlikely that the ASEAN-6 countries will become direct targets for Trump’s tariffs in the short run. Among the countries in the group, Vietnam and Thailand exhibited last year the largest bilateral trade surpluses, at USD 125 Bn and USD 35 Bn, respectively. But the ASEAN-6 countries attract less attention than other major U.S. trade partners with more significant bilateral trade surpluses, mainly China (USD 300 Bn) or Mexico (USD 172 Bn). Furthermore, the Southeast Asian countries are positioned as a counterweight to Chinese influence in the region, leaving them in an favourable stance to face trade negotiations and defuse potential tariff threats.

Second, geopolitical and trade tensions between the U.S. and China are leading to shifts in trade and investment flows that benefit the ASEAN-6 economies. ASEAN exporters that compete with Chinese producers stand to gain from U.S. tariffs on China, as ASEAN producers become relatively cheaper than Chinese products in the U.S. Indirectly, firms in these countries increasingly act as intermediaries for Chinese products to enter the U.S. in order to bypass tariffs. Additionally, ASEAN economies benefit from investments from global companies, including those from China that are more interested in establishing production facilities ouside of China. Western companies are progressively adopting a “anything but China” strategy, aiming to reduce reliance on China and mitigate risks associated with geopolitical tensions. Thus, the ASEAN-6 countries stand to capitalize from trade and investment flows shifting away from China.

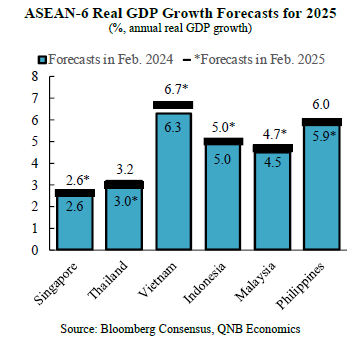

Third, in spite of the worsening international trade outlook, there has been little impact on growth expectations for the highly trade-integrated ASEAN-6 economies so far. Specifically, forecasts for real GDP growth for 2025 have either remained unchanged, or have even shown improvements in the last year. After bringing inflation under control, central banks in the region are driving policy interest rates down, or have already reached “neutral” levels, that neither restrain nor estimulate economic activity.

In several countries, governments are pushing for ambitious pipelines of infrastructure and capital expenditure projects that also draw private investments and bolster economic growth. Major projects are expected in sectors such as transportation, logistics, mining, and facilities needed for new manufacturing plants. Although the specific drivers vary by country in the ASEAN-6, overall growth momentum is expected to remain robust during 2025.

All in all, the outlook for growth in the ASEAN-6 economies has remained largely unharmed by the deteriorating global trade scenario, on the back of still-robust growth momentum, a favourable position to avoid or defuse tariff threats, and the gains from shifting trends in trade and investment flows.

Download the PDF version of this weekly commentary in

English

or

عربي