Uncertainty has been high in recent months on the back of the national election in the US, which was set to determine the fate and policy priorities of the largest economy globally. While most analysts have expected a significant reduction in overall uncertainty after the US election in November, uncertainty remains high. After an ample Trump victory with a Republican “sweep” – control of the Senate and House –, there are now questions whether Trump 2.0 would adopt a “maximalist” approach to controversial proposals, such as tariffs, the fiscal stance and migration. This brings significant consequences for global growth and inflation.

As it is notoriously difficult to read too much into the tea leaves of US politics, particularly before the Trump administration starts, we turn to commodity markets to analyse what the price action from key tangible goods is telling us about the global economy. Commodities provide critical insights into the overall health of the global economy, given their importance for construction, transportation, manufacturing and foodstuff. This includes relevant information for trends on sentiment and inflation, with commodity prices often leading or confirming cyclical turning points.

In our view, prices within the overall commodity complex seem to sustain a benign macro view of stable growth with continuous disinflation, despite recent concerns about Trump 2.0 potentially de-anchoring inflation expectations. Three factors support this position.

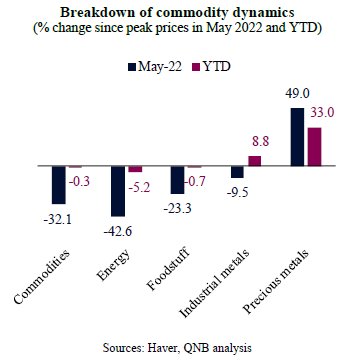

First, broader commodity prices are still significantly below their recent peak in May 2022 but roughly stable on a year-to-date (YTD) basis. This is seemingly challenging both the narratives of a global economic re-acceleration or inflation pick-up and of an impending sharp slowdown. In fact, the price correction from the May 2022 peak without major volatility or resurgence in recent months suggests that the disinflation trend is intact. On the other hand, stable YTD prices point to resilient global consumption and investment. Importantly, the moderate increase of industrial metals YTD, in particular copper, expresses expectations about improving growth conditions in emerging Asia and particularly China, a large consumer of copper.

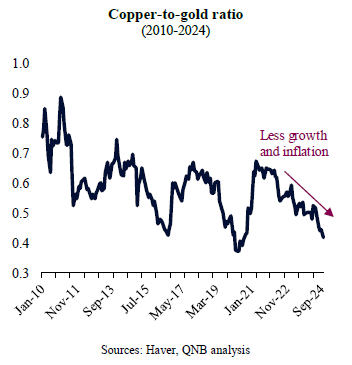

Second, the copper-to-gold ratio, a traditional gauge for growth and inflation expectations as well as risk sentiment, seems to point to a moderate environment over the coming quarters. This comes in contrast to the view that Trump 2.0 would potentially increase both potential GDP and inflation, creating a strong “risk-on” behaviour for investors. Should that be the case, copper prices would have been gaining ground at a faster pace than gold, leading to an increase of the copper-to-gold ratio. Instead, the opposite has been happening. This suggests, if we only consider the commodity markets and its dynamics, an outlook of lower inflationary pressure with moderate growth.

Third, strength in precious metals prices are likely reflecting higher geopolitical risk premium and institutional demand for non-jurisdictional assets, rather than anything more significant related to growth or inflation. Gold prices are close to all time highs, up 42% since May 2022 to close to USD 2,650/troy oz. However, silver prices, key as an input for the new economy (technology and clean energy industries), are more significantly below its recent highs and overall slightly underperforming gold. Should there be a major impulse for higher growth and inflation, silver prices would advance more rapidly than gold.

All in all, despite concerns about Trump 2.0 bringing about unbalanced growth and inflation, commodity prices are suggesting a more constructive scenario of moderate growth and continuous disinflation. Most cyclical commodities are now stable at prices that are significantly below the recent peak, the copper-to-gold ratio continues to decline and gold is outperforming silver, pointing to a lack of pressure from excess overall demand or economic activity.

Download the PDF version of this weekly commentary in English or عربي