Trade is one of the engines of progress, boosting efficiency, productivity and growth. Underpinned by real cross-border flows, global trade is essential to integrate all key markets, including physical consumer goods, capital goods, as well as fundamental inputs, such as raw materials and commodities. Hence, anything that jeopardizes or produces significant changes to trade flows should require the attention of policymakers, analysts and investors.

In recent weeks, US President Donald J. Trump has dominated all the big trade headlines. While there was an initial relief about Trump’s trade stance after his inauguration speech on the 20th of January, this was rather short lived. Earlier this month, the first “trade war” disputes have started: a direct threat of 25% tariffs on Canada and Mexico as well as 10% tariffs on China. This was followed by discussions about “universal tariffs” and “reciprocal tariffs” against all countries and products as well as targeted 25% tariffs on all imports of steel and aluminium. Taken together, these discussions amounted to a significant increase of trade policy uncertainty.

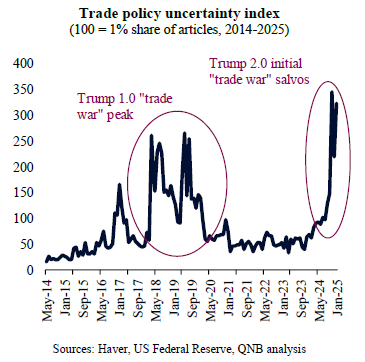

According to the trade policy uncertainty index, which measures the monthly frequency of articles discussing trade policy uncertainty as a share of the total number of news articles across major US newspapers, trade uncertainty is already higher than during the height of the “trade war” with China during Trump 1.0 (2017-2021).

For context, during Trump 1.0, the US average import tariff rose from 1.5% to roughly 3%. Should the new proposed tariffs for North America and China stand, the same average would rise to 11%, the highest ratio since the Second World War.

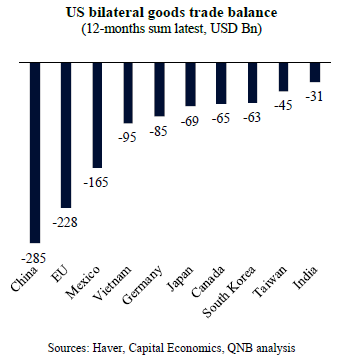

While Canada and Mexico secured a temporary pause in the implementation of new tariffs, uncertainty remains. New trade discussions are set to start with other partners as well. Tariffs on the European Union and additional tariffs on China are expected to be announced soon, further increasing the threat of protectionism and trade wars, particularly as retaliations ensue. Countries and blocs that run a significant trade surplus with the US, such as China, the EU, Mexico, Vietnam, and Japan, are particularly vulnerable to US trade pressures.

Importantly, tariffs are no longer considered only as tools designed to discipline “unfair” trade practices or correct the existing large bilateral imbalances mentioned above, but also as fiscal measures aiming to create much-needed new revenue streams for the US government, i.e., tariffs are tools to raise revenues to the US public purse. This is particularly relevant in a context where Trump’s new economic team intends to find creative ways to fund tax cuts and deliver a significant fiscal consolidation plan, from the existing deficit of over 7% of GDP to 3% of GDP by 2028. In other words, tariffs are now part of the fiscal toolkit and the USD 4.1 trillion of US imports per year should provide a large tax base for the government to tap, helping to narrow the fiscal deficit.

Hence, tariffs and trade disputes are going to be much more central to Trump 2.0 than they were to Trump 1.0. In our view, the new Trump 2.0 administration will further ramp up tariffs already in H1 2025, with several direct and indirect impliactions for the US economy. First, over the short-term, trade tariffs will create a temporary inflationary shock on imported goods and services by the US, also negatively affecting disposable income and thus growth. However, this is a “one-off” shock that should dissipate over a few quarters, as new price levels stabilise. Second, also over the short-term, trade uncertainty is likely to disrupt CAPEX planning by large companies and foreign direct investors, as supply chains need to be re-designed and cost structures re-estimated. This should dampen the optimism of markets, leading to lower investments. Third, over the medium- and long-term, higher tariffs would favour domestic manufacturing and services in the US, but this would come at the expense of consumer’s disposable income, increasing inefficiencies and likely leading to lower potential GDP.

All in all, tariffs are expected to be a cornerstone of the Trump 2.0 agenda, far surpassing the role it played during Trump 1.0. Tariffs are set to increase substantially and in a relatively short period, following the likely use of tariffs as fiscal tools. Over the short-term, this could increase US inflation and reduce investments, whereas on the long-term it should boost domestic producers at the expense of consumers.

Download the PDF version of this weekly commentary in

English

or

عربي