The unexpected full “Republican sweep” in the last US national election in November 2024, when president Donald Trump gained an ample mandate from voters, naturally triggered significant moves from major asset classes. In fact, equity prices, the USD and US Treasury yields have all moved up significantly in recent months.

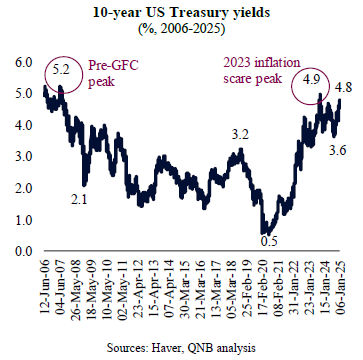

Of all the recent price moves, however, the change in US Treasury yields has been dominating the headlines and investor discussions. 10-year Treasury yields have gone up from 3.6% in September 2024 to 4.8% in mid-January 2025, reaching levels that are close to the peaks last seen briefly only in October 2023 and before the global financial crisis in 2007.

Importantly, the spike in yields is not only limited to the 10-year tenure but can also be seen to some extent across the duration curve, affecting the entire USD 28 trillion Treasury market. This is relevant as the price action of US Treasuries is a critical barometer for understanding macroeconomic conditions, as shifts in yields capture investors’ evolving views on Federal Reserve (Fed) policy, growth, and inflation. In other words, the treasuries provide a real-time signal of market sentiment on the overall health and trajectory of the US economy.

Hence, this piece looks into recent movements in Treasuries to draw some insights about what the markets are telling us about the expectations of the US economy today and in the future. We draw two main conclusions.

First, Treasury markets point now to higher policy rates over the short-term than previously anticipated, suggesting that there is little left for the Fed to cut during this monetary easing cycle, as rates currently stand at 4.5%. A few months ago, short-dated Treasuries were pricing 150 basis points (bps) more cuts to the Fed base rates throughout 2025, whereas it currently implies only 25-50 bps in cuts. The change signals that the Fed will refrain from being too aggressive in its monetary policy easing actions. This also highlights that both growth and inflation are likely to be more elevated than earlier projections indicated.

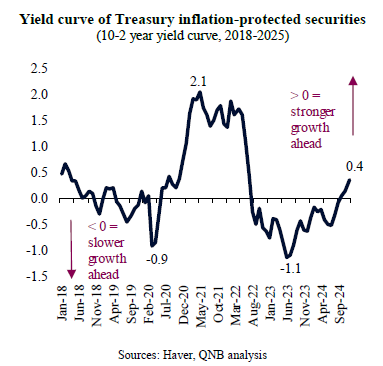

Second, in terms of a longer time horizon, the yield curve has flattened significantly, indicating reflationary expectations, i.e., that higher growth rates are likely in the future, surpassing any effects from inflationary pressures. This can be better observed in the 10-2 year yield curve of Treasury inflation-protected securities (TIPS), which strips out the effects of inflation to directly reflect changes in “real rates.” A steepening real yield curve (where the 10-year yield moves up faster than the 2-year yield) typically signals that investors expect accelerating activity down the road. In recent weeks, the curve had not only steepened but also became positive, with longer-dated yields higher than shorter-dated ones, suggesting that the stagflationary shock that prevailed after 2022 is likely over. It is relevant to compare the difference of the real yield curve currently with what was prevailing in 2023, last time when nominal yields were also high: while then the real yield curve was deeply negative, pointing to weaker growth and higher inflation, it is currently positive, suggesting higher growth and more contained inflation. In other words, we are currently in a more constructive growth environment for the first time since the immediate post-pandemic recovery.

All in all, while Treasuries suggest that the Fed is likely to be more cautious with its easing policies in 2025, yield changes across the curve point to higher growth driving yields up, rather than inflation.

Download the PDF version of this weekly commentary in

English

or

عربي