The global economy continues to benefit from one of the most dramatic economic recoveries in decades. After the Covid-19 shock produced the sharpest and deepest slowdown on record in Q2 2020, aggressive policy stimulus and the temporary containment of the pandemic led to a significant rebound.

While new waves of Covid-19 in Europe, the US and Asia have been slowing the economic recovery process in recent weeks, the development of several effective vaccines provided a powerful tailwind for growth expectation over the near future. As a result, global markets continued to showcase “risk-on” behavior, with equity indices staging strong performances and cyclical commodities paring previous losses or even making new highs.

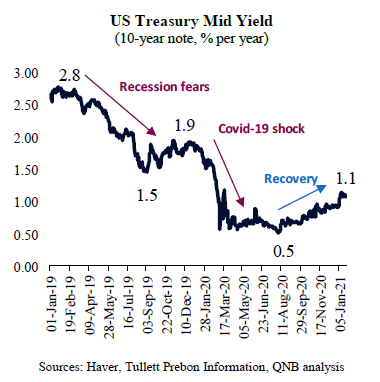

Importantly, macro-sensitive US Treasuries confirmed the positive backdrop. In fact, after recession fears and the Covid-19 shock led 10-year US Treasury yields to decline precipitously for more than a year, the incipient economic recovery started to push yields up after August 2020.

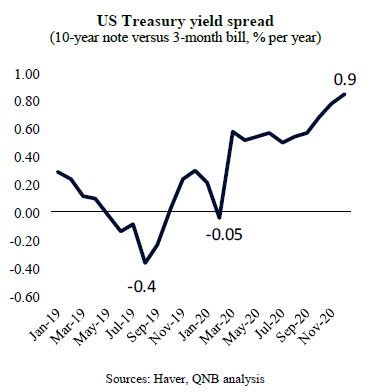

Currently, higher US Treasury yields point to a continuous growth reflation or inflation pick up. The benchmark spread between 10-year and 3-month Treasuries reversed back into positive territory, producing a healthy steepening of the yield curve. This is a leading indicator of economic expansions as lower short yields imply monetary stimulus and higher long yields imply higher growth or inflation expectations.

Despite months of advancing US Treasury yields, we believe that a significant continuation of the upward move in US yields is unlikely to take place over the medium-term. Three factors underpin our view.

First, there is limited scope for inflation-driven yield spikes in the near future. Irrespectively of the recent rise in inflation expectations in the US and abroad, deflationary forces are still dominant over the medium-term. While pandemic-related supply disruptions and sudden changes in consumer behavior produced temporary price distortions, resource utilization remains well below potential. Unemployment is high across most advanced economies and there is no shortage of spare capacity in several industries. It is rare to see sustained price pressures in economies where you have overcapacity of labor and output, given that both wages and the price of goods would tend to go down.

Second, interest rate differentials globally will likely limit more upside movements in US Treasury yields, especially as the US economy continues to outperform other advanced economies. Savers in European countries and Japan, where activity has been more sluggish and interest rates are negative, will likely increase their allocation to US Treasuries should US yields increase further. Given the massive amounts of savings in certain European countries and Japan, this demand should contribute to cap US Treasury yields in the near future.

Third, higher US Treasury yields could be detrimental to the highly leveraged US corporate and government sectors, increasing rollover risks and the overall debt burden. Access to cheap credit is a sine qua non condition to continued fiscal expansion and to the survival of large swaths of the US corporate sector. A higher debt burden in the US would lead to less government support, weaker overall demand and mass bankruptcies. Thus, there is little appetite from US economic authorities to allow for disorderly spikes in bond yields. The US Federal Reserve and the US Treasury will do “whatever it takes” to keep US yields at reasonable levels.

All in all, the increase in US Treasury yields since August 2020 has been positive, indicating investor confidence on the global economic recovery. However, a continuation of such strong movement is unlikely, and would anticipate potential problems ahead, including unanchored inflation expectations, inefficient capital flows and unbalanced credit risks. In our view, US Treasury yields are set to consolidate around current levels, capped by high levels of unemployment and overcapacity, interest rate differentials among advanced economies and the potential for central bank and government intervention in bond markets.

Download the PDF version of this weekly commentary in English or عربي