Although Japan may has been surpassed by China some years ago as the Asian economic dynamo and world’s second largest economy, its relevance remains critical to capital flows and financial markets.

In terms of magnitude and size, Japan is a USD 4.2 trillion (Tn) economy, comprising 3.6% of global GDP adjusted by purchasing power parity, the third largest after the US and China. The country is a major exporter of manufactured goods and one of the most sophisticated nodes of “Factory Asia,” i.e., the integrated supply chains linking the advanced economies of Northeast Asia with the emerging economies of China and Southeast Asia.

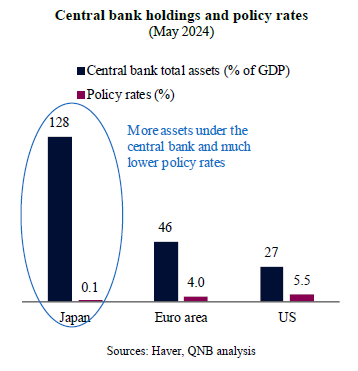

In addition, the country is a global financial powerhouse. Japan’s financial markets play a major role in the global economy as the Japanese Yen (JPY) is a key reserve currency. The domestic Japanese government bond (JGBs) market is also one of the largest global sovereign bond markets, making the JGB yields an anchor for global interest rates. This is particularly relevant as the Bank of Japan (BoJ) has been at the vanguard of ultra-loose monetary policies for years, deploying tools such as negative rates, yield curve control (YCC) and massive asset purchase programmes.

Ultra-loose policies make the BoJ an outlier in terms of overall asset holdings and the Japanese policy rates lower than the ones found in other advanced economies. As a result, Japan operates as a major capital and liquidity provider to the rest of the world. This is due to Japanese investors searching for higher yields overseas and market participants exploring “carry trade” opportunities based on low JPY rates, i.e., borrowing at a low rate in Japan to invest at a higher rate in other jurisdictions, speculating with the interest rate differentials.

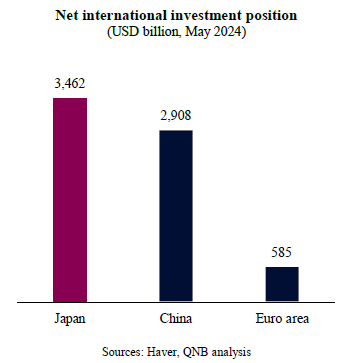

Under these circumstances, it is no surprise that Japanese residents hold the largest amount of net investments overseas, far outpacing both the Chinese and the Europeans.

The general set up of ultra-loose monetary conditions in Japan helped to fund investments overseas for many years. However, since the beginning of 2022 and the emergence of higher than target inflation in advanced economies, risks started to increase, driven by the change in monetary policy direction in the US and Euro area. This triggered capital outflows from Japan, ramping up pressure on the local currency as investors sold JPY to invest globally.

FX pressures on the JPY experienced three phases. First, during the “peak hawkishness” from major central banks in 2022, when inflation was running too high for comfort in the US and Europe. The JPY then depreciated sharply and the BoJ had to intervene in FX markets to prop up the currency and prevent more financial stress.

Second, a period of temporary stabilization in 2023, due to a narrowing of the “policy gap” between the BoJ and its main peers, which supported a JPY flash rally. This was predicated on inflation moderating significantly in the US and Europe at the same time that prices were increasing in Japan. The previous period of JPY weakness triggered a domestic price spiral in Japan that contributed to take inflation above the 2% target into a 41-year high. The BoJ then signalled the beginning of a historical monetary policy normalization process, including the end of negative policy rates and the YCC. With the major central banks signalling the end of their tightening cycle and the BoJ signalling the beginning of its normalization process, the expected “policy gap” narrowed while the JPY strengthened.

Third, a second process of more intense pressure on the currency, which gained momentum in early 2024, following the impact of the earthquake in Japan as well as the re-acceleration of inflation in the US. The earthquake in Japan early this year acted as a catalyst against the JPY, as the need for relief support measures favoured a slower than anticipated process of monetary policy normalization by the BoJ. This new bout of JPY depreciation was further amplified by negative surprises in US inflation and the consequent re-pricing of USD yields. In other words, the “policy gap” widened again. This pushed the JPY to close to all-time lows against the USD in recent weeks, requiring more BoJ intervention to support the Japanese currency.

Importantly, signs of a disorderly depreciation of the JPY are starting to pressure other key parts of “Factory Asia,” such as Korea and China, as regional currency moves affect the competitiveness of each economy. A wave of disorderly depreciations and devaluations in Asia could lead to financial market stress. This is because local monetary authorities would have to tap into their foreign assets to intervene in FX markets, or use regulatory instruments to prevent further capital outflows. As Asian countries are net providers of capital to the global financial system, this would be negative for liquidity, especially as the Fed is positioning itself to keep policy rates “higher for longer “or to cut rates less than previously expected.

All in all, a stabilization of the JPY is important to prevent a larger regional FX crisis, which could have implications for overall global liquidity and growth.

Download the PDF version of this weekly commentary in

English

or

عربي