Lord John Maynard Keynes, arguably the most important economist of the 20th century, had notoriously dismissed gold as a “barbarous relic of the past,” a commodity underpinned by “superstition” and a “primitive passion for solid metal.” In a similar fashion, Ben Bernanke, former Chair of the US Federal Reserve, defined the role of the precious metal in the current economic system as a mere function of “tradition.” Colourful statements from famous detractors aside, gold has been held by investors, households, governments and corporations for millennia. While the commodity does not generate any income stream, it has served as a long-term store of value for generations, protecting portfolios against systematic macro risks such as the Great Financial Crisis of 2008-9.

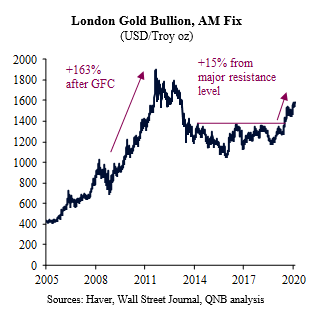

Importantly, gold has recently benefited from a resurgence in demand. As a result, after six years in the doldrums, the precious commodity has broken out from a major resistance level to hover around the current price of USD 1,590 per ounce. Our analysis delves into the three main factors behind higher and rising gold prices.

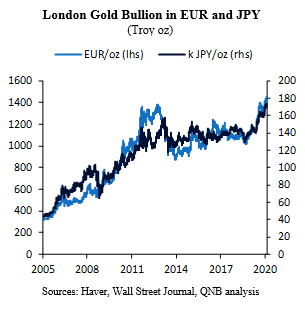

First, the attractiveness of longer-dated government bonds from advanced economies to investors has diminished significantly. As policy rates and yields across the curve reach nominal levels at or close to or even below zero (lower bound in interest rates), investors find little solace on riskless government-backed fixed-income papers. As a result, capital has to either run for riskier securities or search for alternative safe haven assets such as gold. While both high-quality government bonds and gold are defensive assets that tend to rise in value during risk-off environments or negative shocks, the upside for bonds is currently capped by the lower bound in interest rates. Under such circumstances, as negative shocks occur, gold prices are likely to decouple from rates, outperforming them. This is particularly relevant for Japan and Europe, where rates are extremely low or negative. In fact, gold prices in EUR or JPY have already reached all-time highs in recent weeks.

Second, a plethora of high and rising political, geopolitical and other tail risks are threatening global economic conditions, which puts a risk premium in more traditional assets and favours alternative safe havens. Moreover, secular geopolitical trends such as the increasing competition between the US and China, less international cooperation, trade conflicts, nationalism and sanctions are boosting the demand for non-jurisdiction type of safe haven assets such as gold. Purchases of gold by central banks from all continents have reached multi-decade highs in the last couple of years.

Third, low growth, low inflation and low interest rates in a context of increasing social inequality is triggering a demand for additional fiscal spending. While there is currently some fiscal space in certain advanced economies, the rise of populism is also favouring less credible political views about expansive fiscal policies. “Fiscal populists” often propose more government spending to support employment and growth, despite high debt levels. This adds to existing concerns associated with unfunded liabilities (pensions) and the potential need for even higher fiscal deficits in the future. Over the medium term, such policies are conductive to fiscal dominance, i.e., a condition that generally involves government debt monetization with un-tamed inflation and financial repression. Gold tends to soar in such environments and very long-term investors are already starting to position themselves for such scenarios.

All in all, we believe that long-term trends are favouring the return of gold as a diversifier and shock absorber in the portfolio of global investors. We are likely in the beginning of such a movement and the upside is significant for gold prices over a long-term horizon or the coming decade.

Download the PDF version of this weekly commentary in English or عربي