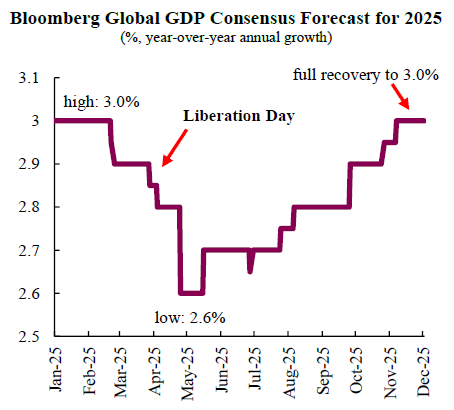

At the beginning of the year, against a backdrop of cautious optimism, the global outlook pointed to steady economic growth of 3%. Tailwinds included continued policy easing from major central banks, resilient growth in the US, and receding inflation in major economies. This was supported by a cyclical recovery in the Euro Area and China. Growth in both advanced economies and emerging markets was initially expected to remain steady at rates that would match those of 2024.

The climate of optimism and positive market sentiment began to shift in February, as the new US administration embarked on an aggressive agenda of policy change. On April 2, a day that later came to be known as “Liberation Day,” President Trump announced unprecedented tariffs for goods entering the US. Markets and macroeconomic expectations experienced significant volatility, on fears of broader and deeper trade wars. The narrative then debated the odds of a world recession. At its worst moment, growth expectations for the global economy dropped from the initial peak at the beginning of the year by 0.4 percentage points (p.p.) to 2.6%, a significant downgrade in a very short period.

But then the prospects began to recover, as policy shocks and trade-related spillovers proved to be more limited than initially expected, with growth forecasts across the world undergoing several rounds of re-calibration. Furthermore, US trade policy shifted towards a more pragmatic stance, reaching an increasing number of deals that helped moderate uncertainty, as well as discard the most extreme negative scenarios for global trade.

But then the prospects began to recover, as policy shocks and trade-related spillovers proved to be more limited than initially expected, with growth forecasts across the world undergoing several rounds of re-calibration. Furthermore, US trade policy shifted towards a more pragmatic stance, reaching an increasing number of deals that helped moderate uncertainty, as well as discard the most extreme negative scenarios for global trade.

In this article, we dive into the factors that drove the recovery of growth expectations during 2025 for the three major economies: the US, China, and the Euro Area, which together account for close to 60% of the world economy.

In the US, a reacceleration of the economy took place on the back of strong momentum in consumption and private investment. Household consumption was underpinned by the combination of still-resilient employment and record household net wealth. Even as job gains have slowed, average unemployment rate of 4.2% this year remained in the range of healthy employment, while earnings have steadily grown in real terms, outpacing inflation. This helped to keep aggregate household incomes strong. At the same time, a positive wealth effect from rising stock markets has bolstered spending capacity.

US business investment also showed a robust performance, on the back of favourable financial conditions supported by monetary easing, fiscal incentives, and technology and AI-related capital expenditures. As a result of steady investment and consumption, a consensus of overall resilience for the US economy emerged towards the end of the year, with growth expected at close to 1.9% in 2025, a notable recovery of 0.6 p.p. from the low registered mid-year.

US business investment also showed a robust performance, on the back of favourable financial conditions supported by monetary easing, fiscal incentives, and technology and AI-related capital expenditures. As a result of steady investment and consumption, a consensus of overall resilience for the US economy emerged towards the end of the year, with growth expected at close to 1.9% in 2025, a notable recovery of 0.6 p.p. from the low registered mid-year.

In the Euro Area, the economy showed remarkable resilience despite the headwinds from US tariffs, the energy crisis, the war in Ukraine, and intense competition from China. As inflation was brought under control, the European Central Bank (ECB) has lowered its benchmark policy rate by 200 basis points (b.p) from a highly restrictive level of 4% in mid-2024, to 2% by June this year. This brought the policy rate to a range that is no longer restraining economic activity. In addition to lower interest rates, private consumption was supported by sustained growth of wages adjusted for inflation, as well as still-firm job creation. The Recovery and Resilience Facility (RFF) and other EU funds continued to back investment by firms, while the recent tariff-shock proved to be manageable with limited impact on competitiveness. Despite the accumulation of economic headwinds, end-year consensus sees the Euro Area growing more than initially expected after years of weak activity.

In China, robust growth was driven by positive momentum from a turnaround in the private sector, bolstered by a more supportive economic policy mix, optimism around the country’s AI capabilities, and a stabilization in manufacturing activity. This came after years of subdued investor appetite and volatile growth on the back of manufacturing and real estate oversupply, regulatory stringency, limited official stimulus, and the trauma from hard pandemic lockdowns. The turnaround overlaps with the transition of the Chinese economy from exporting simple consumption goods to exporting advanced-technology manufacturing, and high value-added products, a process that is re-positioning China at the high end of global supply chains. Despite the external shock from trade disputes with the US, the consensus growth forecasts for the Chinese economy improved relative to initial estimates, anticipating an expansion of close to 5% for the year.

All in all, the three major economies showed notable resilience during 2025 against significant turbulence and major negative shocks. End-year forecasts for China and the Euro Area are better than at the beginning of the year, while they only slightly worsened for the US, adding up to a global economy expansion of 3%.

Download the PDF version of this weekly commentary in English or عربي