Positive expectations prevailed around Japan’s economic outlook at the end of last year. This was a remarkable sign of confidence given the less favourable external context represented by a global economic slowdown that was becoming a headwind for the world’s 3rd largest economy after the US and China.

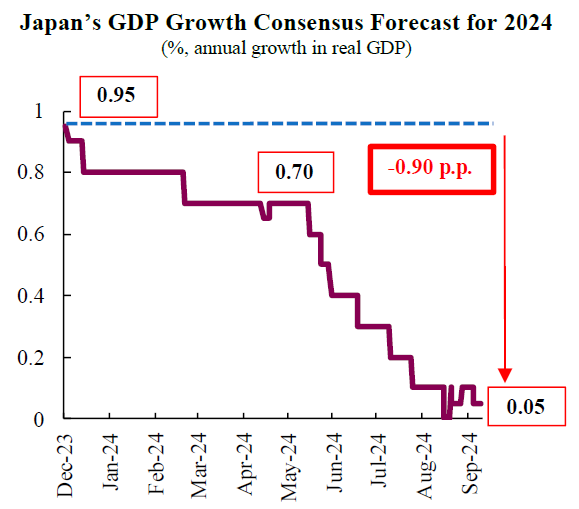

The Bloomberg survey consensus is a useful tool that tracks the evolving views over major macroeconomic developments. This benchmark survey records forecasts from analysts, think tanks, and research houses. At the end of last year, the consensus showed that the expected pace of real GDP expansion stood at 0.95% for 2024, encouragingly above the 0.75% annual average for Japan since 2000. However, this relative initial optimism began to deteriorate as sentiments shifted with the earthquake that hit the Asian country on New Year’s Day, followed by leading indicators that pointed to softening economic activity.

In Q2-2024, real GDP was barely 0.1% above the pre-pandemic peak reached in Q3-2019, implying that the economy had barely advanced over the last five years. By September, growth expectations for the year had fallen to just 0.05%. In this article, we discuss three key factors that explain the dramatic shift in expectations for Japanese economic growth.

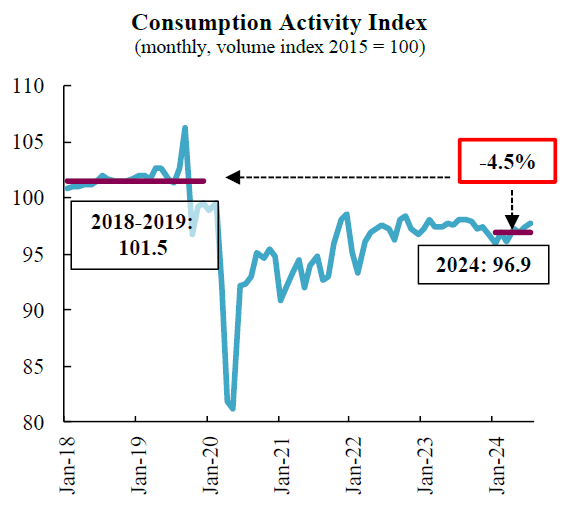

First, stagnating consumption remains a significant drag on economic growth. Consumption represents approximately 60% of the Japanese economy, and is therefore a major factor in determining its performance. In spite of a strong post Covid-pandemic recovery, consumption has been in uninterrupted year-over-year decline since December last year. Furthermore, average consumption this year has remained on average 4.5% lower than the pre-pandemic average during 2018-2019, and 0.4% below the level of 2023.

The main reason for weak consumption growth lies in high inflation rates that led to an erosion of the purchasing power of salaries, weighing on household expenditures. In July, workers’ earnings adjusted for inflation grew 0.4% year-over-year, but this offers very little relief after an extended period of negative growth rates, and real earnings earnings that are still 2% below the peak in 2022. In addition, an aging population adds to the negative factors affecting consumption. Older Japanese consumers are more conservative with their spending compared to younger generations, and tend to prioritize savings, given their dependence on pension income and a higher weight of their expenditures on essentials like healthcare. Given the importance of consumption, these negative trends are dragging the performance of the Japanese economy.

Second, subdued external demand implies weaker support for economic growth of the highly globally-integrated Japanese economy. Protectionist policies and trade barriers continue to build up steadily at the global scale amid rising geopolitical tensions. In addition, with the end of the Covid-pandemic, consumption patterns began a process of normalisation towards services and away from goods, leading to a persistent world manufacturing recession. In this context, global trade growth this year is expected at 2-3%, close to half the average rate during 2000-2022. This outlook for trade added to the pessimism for the Japanese economy, where exports represent 20% of GDP, and are a key driver of industrial production. So far this year, Japanese exports adjusted for changes in prices have fallen 1% relative to last year. Given its importance for Japan, the slowdown in global trade growth represents a major headwind for its economic performance.

Third, low investment rates are hampering Japan’s GDP, as business remain cautious to commit capital expenditures amid global economic and geopolitical uncertainty and weak domestic demand. In addition to sluggish consumer spending, Japan's aging population and labor shortages further limit the potential for high returns on investment, dampening overall economic expansion. Investment levels have fallen by 0.4% in the first semester 2024 relative to the same semester last year. Given that investment represents 25% of the Japanese economy, underwhelming capital spending is restraining the pace of economic growth.

All in all, we expect real GDP in Japan to remain unchanged this year amid a challenging outlook of stagnating consumption, weak external demand and falling investment.

Download the PDF version of this weekly commentary in English or عربي