High inflation is a global trend. Strong demand and supply chain disruptions have pushed up prices in many countries by more than expected only a few months ago. Indeed, inflation is at multi-decade highs in the US, UK, Germany and other advanced economies. However, supply chain disruptions have an impact on the UK more than most countries due to the impact of Brexit, which has resulted in an acute shortage of labour supply, e.g., truck drivers.

Consumer prices in the UK were 4.2% higher in October than a year earlier. This is the fastest rate of inflation for a decade, twice what the Bank of England (BoE) forecast six months ago and more than double its inflation target of 2%. This will have made uncomfortable reading for the members of the BoE’s Monetary Policy Committee (MPC). It should therefore be no surprise that the MPC’s rhetoric has become more hawkish recently.

However, we believe that the MPC are “talking tough”, so that they can act gently with a single symbolic 15 basis points (bp) rate rise in the near future. We expect this to come in February when the BoE publishes its next quarterly Monetary Policy Report (MPR) and will also hold a press conference to help explain the move. We consider a rate rise in December unlikely because the BoE has never raised interest rates just before Christmas since it became independent from direct government control in 1997.

Three key points support this view for interest rate rises in the UK: Inflation is expected to peak in April 2022, driven by one-off factors, before falling sharply by 2023; Quantitative Easing (QE) is already being unwound from the end of the year; and fiscal stimulus is starting to be withdrawn.

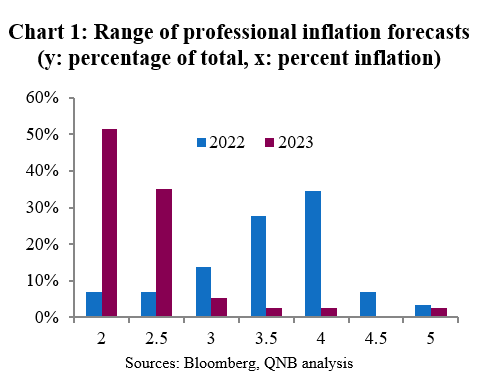

First, we expect further rises in CPI inflation to a peak in early 2022. The combination of the reversal of the VAT cut for the hospitality sector, increases in the energy price cap and rising global goods prices are set to push CPI inflation to a peak of 5% in April 2022. These are all temporary factors that are not expected to push up on future inflation, so we expect the pick-up to prove transitory, with inflation set to ease substantially by the start of 2023. Indeed, our view is shared by most other professional forecasters with the most common forecast for average CPI inflation falling to below 2% in 2023 down from around 4% in 2022 (Chart 1). These widely held views are similar to the BoE’s own view as expressed in its November MPR, in which inflation is expected to remain below 3% in a scenario where the MPC doesn’t raise rates at all. This is the MPC’s way of signalling to markets that only modest rate hikes are needed, if any at all.

Second, the BoE’s QE program will begin to be unwound, with asset purchases of GBP 3.4 Bn per week due to cease by the end of the year. Further, the MPC has provided forward guidance that it expects to stop re-investing the proceeds from maturing bonds once interest rates reach 50 basis points. The tapering of QE and forward guidance are ways that the MPC has already gently begun to tighten policy.

Third, fiscal stimulus is starting to be withdrawn, with the furlough scheme and a temporary uplift to universal credit having already ended. That said, the recent Budget did reduce the scale of fiscal tightening planned for the next two years. Even so, gently tighter fiscal policy will help to reduce the domestically generated contribution to inflation.

These three points support our view on UK inflation; that it will come back comfortably to within 1% of the MPC’s 2% target.

The MPC have demonstrated time and again that they will look-through temporary “first-round” supply shocks to inflation, only reacting when there is clear evidence that there are “second-round” effects (such as excessive wage growth). This pragmatic approach to policymaking has helped to maintain the MPC’s credibility, whilst at the same time maximising the policy space available to keep rates low and support growth.

Other countries have slightly different inflation targets and risks to the outlook for inflation. We perceive a common theme amongst major central banks. They are all making the most of the credibility achieved by three decades of successful inflation targeting. That will help them keep interest rates lower for longer.

Download the PDF version of this weekly commentary in English or عربي