Introduction

The coronavirus outbreak is seriously disrupting economic activity in many countries and has significantly affected global financial conditions. The outbreak has quickly spread around the world and is now seriously impacting the United States.

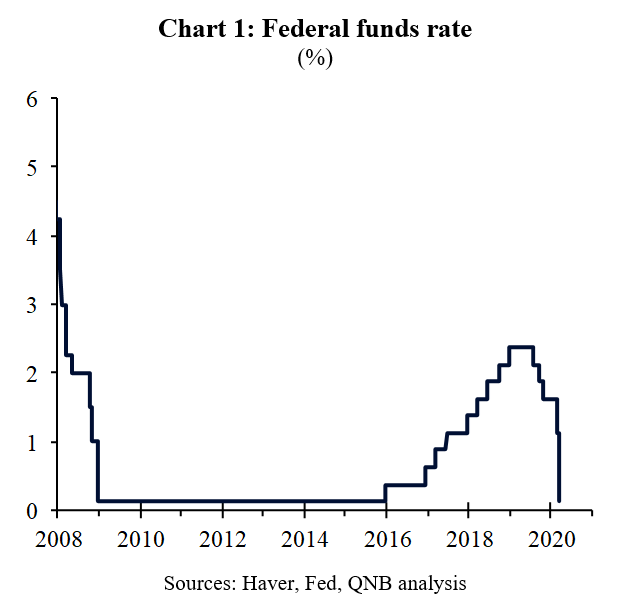

On the 15th March the Federal Reserve (the Fed) first responded with another emergency cut to interest rates, effectively lowering them to zero. Second, the Fed also undertook a related set of actions to provide liquidity including at least an additional USD 700 billion of quantitative easing (QE). Third, the Fed made adjustment to its open market operations and returned to crisis management tools used in 2009.

This week we will explain why the Fed needed to do more than simply cut interest rates to zero and how these additional measures help to support the economy at these difficult times.

Zero interest rates

Monetary policy works by raising, or lowering, the cost of credit for households and business. The Fed’s main tool for implementing monetary policy is its policy interest rate, the federal funds rate (Chart 1).

The easiest way to think about monetary policy is like driving a car. Lowering rates is pressing your foot down on the accelerator, whilst raising rates is switching your foot to press on the brake pedal. In such a simple model, cutting interest rates to zero is having your foot to the floor on the accelerator.

During the 2008 global financial crisis, interest rates hit their zero lower bound and financial markets fell into a liquidity trap. The financial system became dysfunctional when banks become too uncertain about the solvency of counterparties. In such circumstances the Fed must turn to additional tools to ease monetary policy and more directly provide credit and liquidity to households and business. These additional tools include the introduction of quantitative easing, adjustments to open market operations and crisis management tools.

Quantitative easing

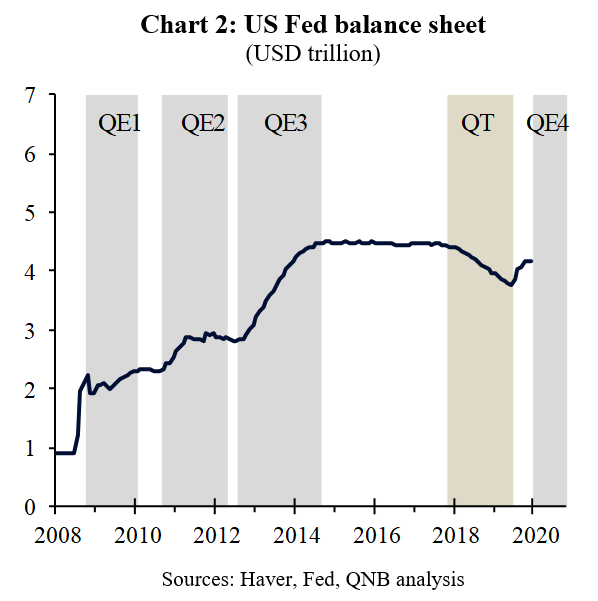

QE involves the Fed purchasing financial assets, with purchases spread over many months and focused on bonds with longer maturities. QE aims to lower long-term borrowing costs.

The Fed launched three QE programs (QE1, QE2 and QE3) in response to the 2008 global financial crisis (Chart 2). On the 15th March the Fed launched Q4 stating that it would increase its “holdings of Treasury securities by at least $500 billion and its holdings of agency mortgage-backed securities by at least $200 billion” without specifying over what time period.

Open market operations and crisis management

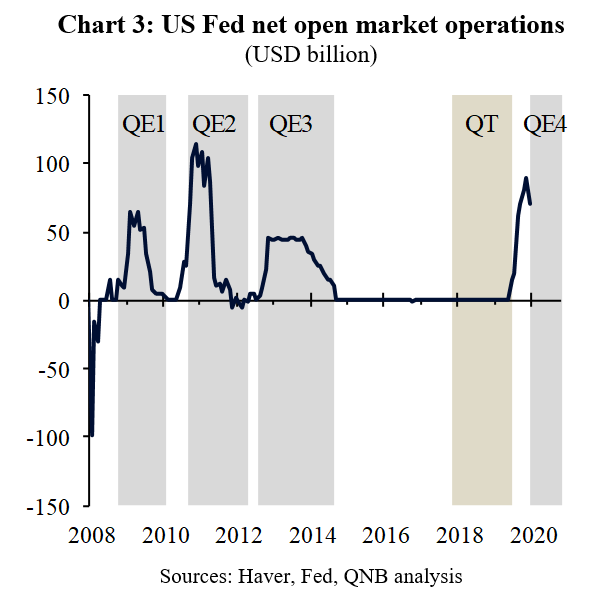

The Fed sets the federal funds rate by controlling liquidity in the US banking system through open market operations (OMOs). However, in its normal OMOs the Fed only deals directly with 24 “prime brokers” who then provide liquidity to the broader financial system.

Direct operations involve the Fed buying or selling short-term government securities. Repurchase operations or “repo” involve the Fed lending money secured against collateral securities.

The Fed also engages in foreign exchange operations, typically via foreign exchange swaps with other central banks, to provide USD liquidity to foreign banks.

A period of quantitative tightening (QT) and balance sheet “normalization” in 2018 led to spikes in over-night interest rates. The Fed responded in late 2019 by increasing the amount of liquidity it provided via normal OMOs (Chart 3).

From the 12th March the Fed has committed to offer up to USD 5 trillion of liquidity via normal OMOs. However, the level of volatility in financial markets in the past week has prevented liquidity from spreading effectively around the financial system to households and corporates.

Therefore, on the 15th March the Fed also announced a reduction in the cost to banks of accessing liquidity via its discount window. This is important as many smaller banks are not qualified to participate in normal OMOs and only have access to the Fed’s discount window.

In addition, on the 17th March the Fed and US Treasury collaborated to set up a special purpose vehicle (SPV) that will provide up to USD 1 trillion of liquidity. The SPV will provide liquidity secured against a wider range of collateral, including stocks and corporate securities with appropriate haircuts.

By the 18th March, the Fed had already injected over USD 1 trillion in liquidity.

Conclusion

It is clear that with these measures, the Fed is actively engaged in preventing the coronavirus outbreak from causing a full blown financial crisis. Fortunately, the Fed has a wide set of tools, plenty of experience and unlimited capacity to support the financial system. However, the Fed’s monetary stimulus will only become fully effective once governments have brought the coronavirus under control. The monetary stimulus will be further enhanced by the effective implementation of the USD 1 trillion fiscal response that was announced on the 17th March.

Download the PDF version of this weekly commentary in English or عربي