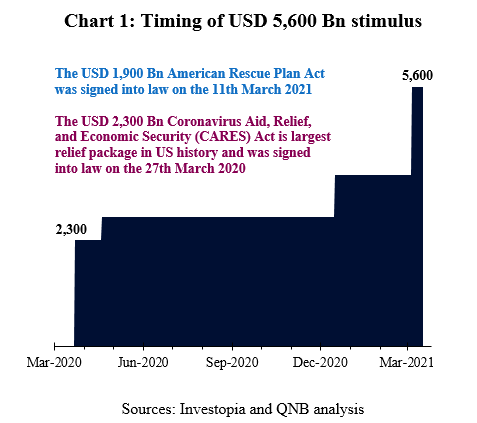

US President Joe Biden signed a new round of fiscal stimulus into law on the 11th March 2021. This latest round of stimulus takes the total amount of pandemic-related spending to around USD 5,600 Bn since the start of the crisis, with half of the stimulus passed since December (Chart 1).

The USD 1,900 Bn package is large, despite economic surveys and data indicating a strong start to the year. In January, retail sales were already 7.4% higher than a year earlier, boosted by many Americans receiving USD 600 stimulus cheques from the government. In February, the US composite PMI rose to a seven-year high and payrolls increased by 379k employees, indicating strong GDP growth.

American consumers are estimated to have accumulated USD 1.6 trillion in cash savings over the past year, through stimulus cheques, unemployment benefits and tax credits. They have been stuck at home and unable to spend as much as normal. Spending on recreational activities including restaurants, bars and cinemas fell the most. Whereas, spending on necessities, like groceries, was more stable, and spending on electronics and online entertainment actually increased.

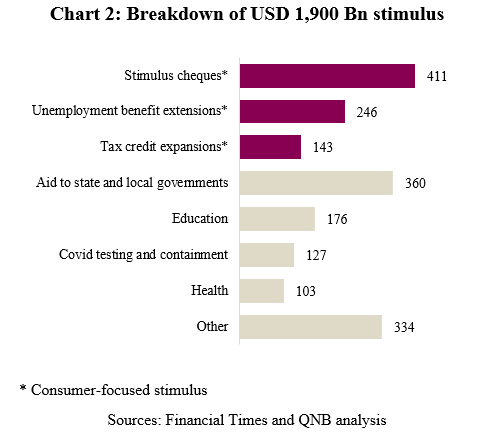

Stimulus checks (worth USD 411 Bn) and unemployment benefits (worth USD 246 Bn) will maintain the consumer-focus of stimulus measures. This will result in a further increase in the share of the cash savings held by low-income households, who are more likely to spend relative to middle class households, once the economy fully reopens (Chart 2). Therefore the, already strong recovery of the US economy is likely to be further accelerated by robust consumer demand growth throughout the year.

We expect the economic boost from further fiscal stimulus to have three key implications.

First, positive spill-over effects to the rest of the world from stronger US demand for imports of energy, raw materials and consumer goods. Strong US import demand will be a particular benefit for the exports of trading partners in Europe, Asia and Latin America. It will also help to maintain upward pressure on global commodity prices, given the size of the US economy, despite weaker outlooks in Europe and Developed Asia. Indeed, in the OECD’s latest forecast the US economy is expected to be larger at the end of 2022 than had been forecast before the pandemic, a unique achievement amongst its peers.

Second, Further upward pressure on the yields of longer-dated US government bonds through both real yields and higher inflation expectations. A stronger growth outlook raises investor’s expectations of future real interest rates. It also raises their expectations of future inflation, especially as the Fed has now moved to a more flexible mandate targeting both “average inflation” and full employment. We expect the Fed to resist pressure to take drastic action, although some more moderate measures may be taken to limit the rise in yields. In our view, the Fed will likely resort to a combination of “twist” operation and “duration extension” to the existing asset purchase program.

Third, increased criticism of the Fed from both sides. Dove-ish critics will argue that the Fed should offset the tightening of financial conditions caused by higher yields through further asset purchases. Whereas, Hawk-ish critics will point to the energy price induced spike in headline inflation and likely strengthening of core inflation in the US to argue that the Fed should bring forward its plans to taper asset purchases. We argue that higher inflation is a positive indicator of economic recovery, which offers hope that, unlike Europe and Japan, the US may be able to escape the low-growth, low-inflation trap that it has been stuck in since the 2008 global financial crisis.

We expect US policymakers to maintain both fiscal and monetary stimulus until economic recovery is on a firm foundation. Continued progress vaccinating the population, should allow lockdown measures to continue to ease during the rest of the year and unleash a torrent of pent-up consumer demand. A strong recovery is more likely to help the US economy avoid a low-growth, low-inflation trap than it is to lead to uncontrollable overheating. Indeed, we expect a strong US recovery to be a positive driver for the global economy. Tailwinds from stronger US demand for imports will likely dominate headwinds from rising yields and higher commodity prices.

Download the PDF version of this weekly commentary in English or عربي