At the beginning of the year, optimism shaped the outlook for economic growth in Japan. The expected pace of real GDP expansion for 2024 stood close to 1%. Even if not impressive by cross-country comparisons, this was encouragingly above the 0.75% annual average for Japan since 2000. The relative optimism gradually faded throughout the year, amid a challenging context of weak external demand, stagnant consumption, and geopolitical uncertainty. Recent forecasts even point to a slight contraction of the Japanese economy for this year. However, headwinds are easing, and conditions are becoming more favourable for the Asian country.

In our view, economic growth in Japan is set for a moderate rebound next year. In this article, we discuss three key factors that will contribute to a better performance for the Japanese economy in 2025.

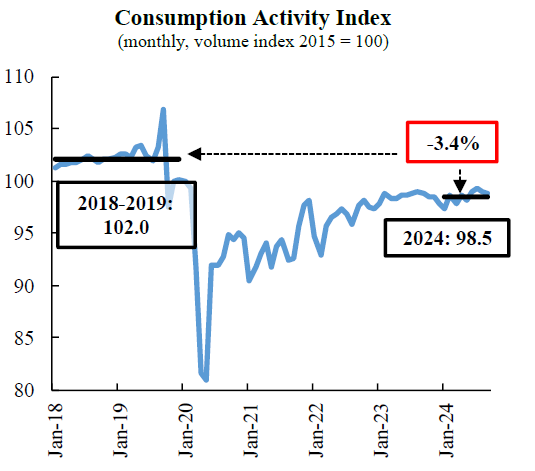

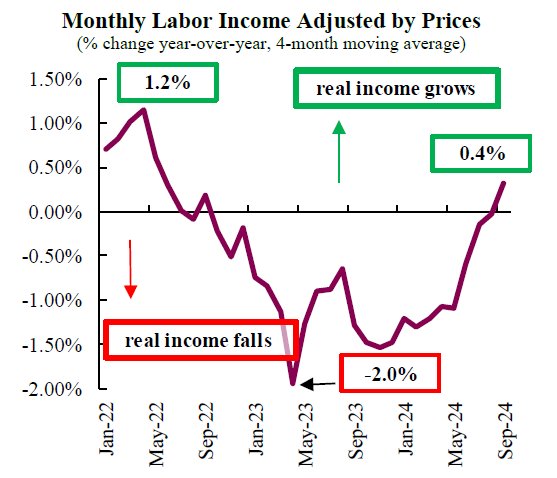

First, robust wage growth is set to outpace inflation, boosting income in real terms and fuelling a recovery in consumption. High inflation has eroded the purchasing power of household income during the last two years. As a result, consumption has stagnated, remaining significantly below the pre-pandemic average during 2018-2019. Since mid-year, growth in wages adjusted for prices began to recover, on the back of the shunto agreement – the yearly negotiations between labor unions and corporate leaders – that led to average wage increases of 5.6%, the largest in 33 years. In Q3 this year, consumption grew at a surprisingly strong annual rate of 3.6%, the highest since the post Covid-pandemic recovery.

Going forward, the largest labor union federation aims to reach an agreement that would deliver a wage increase similar to the previous one. Average wage gains of 5% with inflation running closer to 2% would imply a substantial increase in the purchasing power of households. Prime Minister Ishiba is supporting the wage increases, seeking to bring the economy to a virtuous cycle of growth with stable inflation. Given that consumption represents approximately 60% of the Japanese economy, the boost provided by real income represents a strong support to economic growth.

Second, the government has put forth new policy initiatives and a fiscal program that will provide further stimulus to the economy. In November, the Cabinet approved a JPY 21.9 Tn (USD 140 Bn) package that includes inititatives to mitigate the impact of inflation on household spending, as well as to increase investment in key industries. The measures include cash transfers to low-income households, subsidies for electricity and gas bills, as well as raising the annual tax-free salary threshold to encourage workforce participation, especially among women.

The government is also targeting an increase in investment, with support to capital expenditures in artificial intelligence and semiconductor industries, in a bid to regain competitiveness of the Japanese economy. In the first three quarters this year, investment has grown by only 0.2% relative to the same period last year, an underwhelming pace of capital spending that is restraining long-term economic growth. The new measures by the government will help bolster aggregate growth.

Third, export oriented sectors will benefit from the depreciation of the yen and improving external demand. This year, the yen has depreciated by 7.6% on average relative to last year; a weaker yen enhances the competitiveness of export-oriented industries by making goods and services more affordable on the global market. This currency shift has notably benefited tourism, now one of Japan's largest export sectors. In October 2024, Japan welcomed a record number of 3.3 million visitors. Over the past 12 months, tourist spending reached approximately USD 37.7 Bn, underscoring the sector's substantial contribution to the economy.

Beyond tourism, industries such as automotive and electronics are experiencing increased demand due to better price competitiveness. Additionally, exports will benefit from improving external demand: we expect growth in global trade volumes to continue to recover, accelerating to 3.2% in 2025, from an expected 2.8% this year. Altogether, an improving outlook for export oriented sectors will add to the economic growth recovery in Japan.

All in all, economic growth in Japan is set for a recovery next year, on the back of real income growth boosting consumption, fiscal stimulus and an improving outlook for export oriented sectors. We expect the Japanese economy to grow 1.3% in 2025. This recovery will give room to the Bank of Japan to resume policy rate increases after a cautious hike in March, the first in 17 years.

Download the PDF version of this weekly commentary in

English

or

عربي