We started the year with a constructive view for emerging markets (EM) in 2020. Bullish investor sentiment triggered a powerful risk-on market environment in late 2019, driven by a favourable combination of moderate global growth, high employment and low inflation. China, in particular, was expected to be a key driver of an upcoming economic acceleration, with policy support spilling over to commodities and other open economies.

But bad news spreads fast and far. A “black swan” event materialized in the form of a global pandemic of pneumonia-like virus Covid-19. In the most affected countries in Asia, Europe and North America, the fallout produced unprecedented negative shocks on both the supply side and demand side of the economy. As a result, the outlook changed dramatically. The global economy is now expected to head into the sharpest and deepest slowdown since the post-World War II demobilization of the late 1940s.

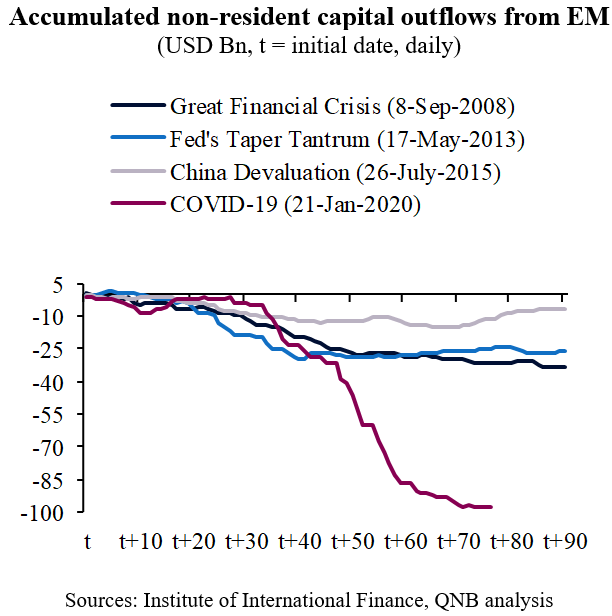

Markets have already started to discount the new scenario with a significant tightening of global financial conditions. Vulnerable EM are being hit hard. According to data from the Institute of International Finance, the Covid-19 shock produced the greatest reversal of capital flows ever, far outpacing other major episodes of EM stress. From late January to early April 2020, non-resident portfolio outflows from EM nearly reached USD 100 billion. The sell-off was mostly concentrated on Asian countries and large EM, including Taiwan, South Korea, Thailand, Brazil, Mexico and South Africa.

Importantly, the demand shock quickly spilled over to commodity prices, in a move that was amplified by diplomatic events such as the sudden end of the OPEC+ agreement. This increased the pressure on commodity producing EM through a deterioration of fiscal, terms-of-trade and current account dynamics. The Bloomberg Commodity Index is down more than 20% while the price of Brent crude is down almost 50% from the beginning of the crisis to the time of writing.

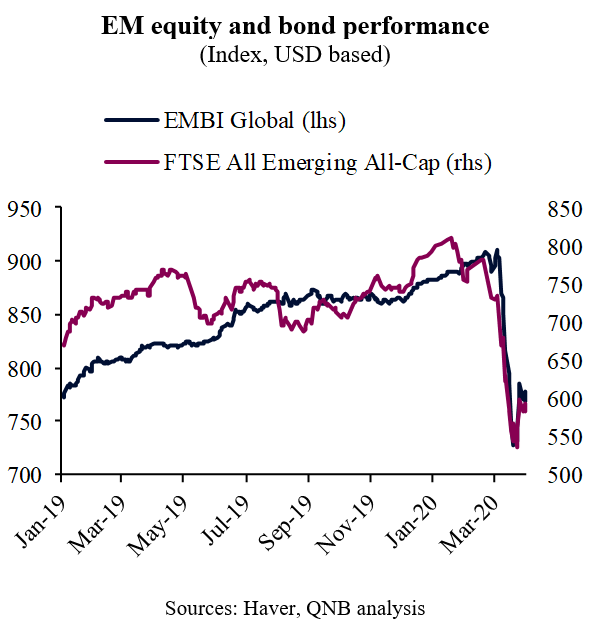

The FTSE All Emerging All-Cap, which is a market-capitalization weighted index representing the USD performance of large, mid and small cap EM stocks, collapsed more than 25% since late January. The J.P. Morgan EM Bond Index (EMBI) Global, the most comprehensive EM debt benchmark covering USD denominated Brady bonds, Eurobonds, traded loans and local market debt instruments issued by sovereign and quasi-sovereign entities, declined by more than 10% during the same period. Volatility spiked sharply.

The rout was so acute that the US Federal Reserve (Fed) had to act. In mid-March, the Fed established temporary dollar liquidity-swap lines of USD 60 billion each with the central banks of Brazil, South Korea, Mexico and Singapore. Not long thereafter, as the demand for USD cash continued, the Fed launched a new repurchase agreement (repo) facility aimed at supplying foreign central banks with USD liquidity through swaps backed by US Treasuries. The measures intend to help ease the strain in global USD funding markets while supporting the smooth functioning of the US Treasury market.

Liquidity support measures and additional policy stimulus are contributing to an incipient stabilization of markets. However, three reasons suggest that EM countries are not out of the woods yet. First, the global economic situation is expected to get worse before it gets better. Covid-19 mitigation strategies should continue to limit activity in the coming months.

Second, disruptions in global trade and supply chains as well as demand destruction in China are particularly threatening to Asian and commodity exporters. Lower export revenues are likely to increase external financing needs in USD.

Third, the deflationary shock from a collapse in global demand is already prompting EM central banks to cut policy rates. In contrast to the US, Europe or Japan, monetary authorities in most EM countries still have some policy space. Lower yields in EM are likely to encourage further capital flight towards safer assets.

The economic consequences of the Covid-19 pandemic will have a deep effect on vulnerable EM. Existing support from the US Fed is necessary but not sufficient to provide a backstop to a broader range of EM. Appropriate global policy responses would include actions to strengthen international financial institutions mandated to support countries with balance of payment problems.

Download the PDF version of this weekly commentary in English or عربي