Gold occupies a unique role in modern investing. It generates no cash flow, incurs storage costs, and has limited industrial utility – yet it continues to hold enduring appeal among households, sovereigns, and institutional investors. Gold’s historical legacy as a monetary anchor has recently intersected with a more contemporary function: risk mitigation. This demand for gold has been supported by the idea that the yellow metal provides a key utility as a portfolio diversifier protecting against inflation, financial crisis, international conflicts and civil strife.

Importantly, gold’s resilience in the face of economic shocks, such as the Great Financial Crisis (GFC) of 2008-09 or the Covid-19 pandemic, underscores its role as a hedge against systemic risks and macroeconomic instability.

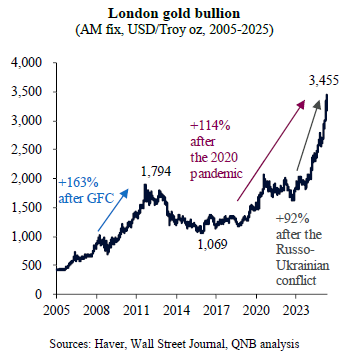

In recent years, gold has rallied significantly, a process that has accelerated over the last few months. In fact, before the most recent pullback, gold prices reached USD 3,500 per ounce, making sequential all-time highs for months.

After such significant rally, which amounts to 114% in price appreciation since the pandemic and 92% since the Russo-Ukrainian conflict began, it is natural that analysts and investors would question whether there is still more upside for gold over the coming years.

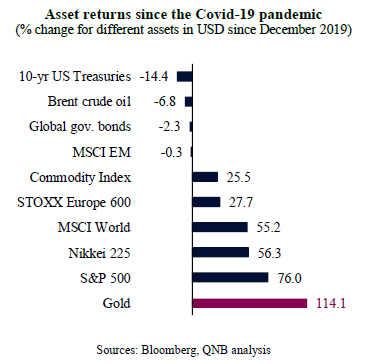

In fact, gold has decisively outperformed all major asset classes, challenging the perception that it merely serves as a defensive hedge. A sustained outperformance highlights that gold, while traditionally valued for its safety during crisis, can also generate robust returns under different macroeconomic conditions. Gold’s consistent gains relative to equities, bonds, and commodities since early 2020 suggest that it merits consideration not only as protective allocation but as strategic, return-enhancing asset within a diversified portfolio. This dual characteristic – providing resilience during uncertainty while also delivering meaningful capital appreciation during periods of higher investor risk appetite – further strengthens the case for gold as a core holding. This is especially valid for environments of elevated inflation, currency de-basement, foreign exchange depreciation, or systematic market volatility.

In our view, despite the surge in prices, there is still further upside for prices over the medium-term, as global macro conditions are favourable for gold. Two main factors sustain our position.

First, gold’s appeal has been further bolstered by secular or long-term geopolitical trends, including the intensifying economic rivalry between West and East, a decline in international cooperation, escalating trade disputes, increasing political polarization, and the “weaponization” of economic relations via sanctions. This has particularly intensified after the Russo-Ukrainian conflict and the US-driven “trade wars.” In an era marked by more geopolitical instability, gold’s status as a tangible, jurisdictionally neutral asset that can serve as collateral in various markets becomes increasingly significant. Reflecting this movement, central banks globally have been accumulating gold at a rate unseen in generations. According to the World Gold Council, after the Russo-Ukrainian conflict in 2022, central bank additional demand for gold more than doubled from 450 tons per year to more than one thousand tons per year. Surprisingly, despite the increase in official demand for gold from central banks, there is still a lot of room for a much longer process of gold accumulation or portfolio rebalancing towards the precious metal. While large advanced economies tend to hold around 25% of their foreign exchange (FX) reserves in gold, large EM-based central banks hold only less than 8% of their FX reserves in gold. Given that these EM-based central banks hold around USD 6 trillion in FX reserves, there is scope for a continued multi-year process of portfolio rebalancing from these reserve managers. This supports a steady long-term institutional demand for gold.

Second, foreign exchange (FX) movements are poised to lend additional support to gold prices. Historically, gold has shown a strong inverse correlation with the USD – typically rising when the USD weakens and falling when it strengthens. The USD has already depreciated by more than 6.9% against a basket of major currencies so far this year. Moreover, despite this sharp depreciation, currency valuations still suggest that the USD remains overvalued by more than 15%, indicating further room for depreciation ahead. A softer USD is likely to support gold prices going forward, as it enhances global purchasing power for USD-denominated commodities like gold, stimulating demand and providing an additional tailwind for prices. Moreover, as investors seek protection against the erosion of purchasing power associated with USD depreciation, they often turn to gold as an alternative store of value. Consequently, a declining USD typically drives higher demand and upward price momentum for gold.

All in all, despite the sharp rally in recent months, there is still further upside for gold over the medium-term. This is supported by strong momentum across different macro regimes, long-term geopolitical trends with central bank portfolio rebalancing, and FX movements.

Download the PDF version of this weekly commentary in

English

or

عربي