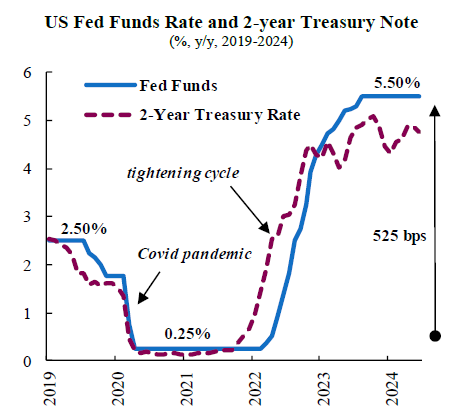

Forecasting policy rates in the US has been a challenge in recent quarters, after the aggressive monetary policy tightening stabilised with rates at 5.5%. This was due to significant volatility in both growth and inflation expectations.

In fact, from late 2023 to early 2024, after a sequence of lower-than-expected inflation prints and weaker GDP growth, markets started to weigh an aggressive schedule of rate cuts. At peak “dovish” expectations in January, markets were pricing close to 200 basis points (bps) in policy rate cuts for this year.

But conditions changed markedly throughout the year as three consecutive months of high inflation prints fuelled concerns regarding the disinflation path. This, alongside higher growth expectations, led to a significant re-pricing of short-term interest rates, which were then expected to remain “higher for much longer.” Some analysts and investors even considered the possibility of further rate hikes to prevent a sustained re-acceleration of inflation.

After the latest round of “inflation scare,” softer data for growth and inflation in recent weeks are suggesting that the US Federal Reserve (Fed) should start cutting rates sooner rather than later, kick-starting the monetary policy easing cycle. In our view, the Fed will have room to cut rates at a faster pace than markets are currently expecting, particularly next year. Three main factors sustain our outlook.

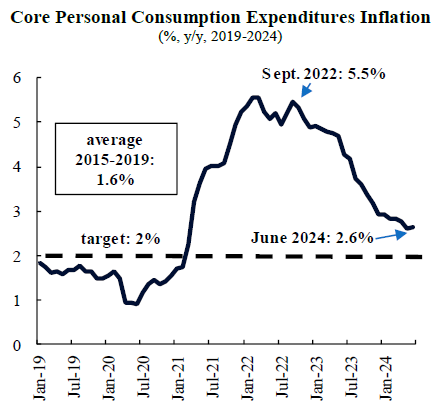

First, the disinflationary trend in the US is intact and could accelerate further over the coming quarters, reaching the Fed’s 2% target earlier than previously anticipated. The disinflationary trend has been grounded on supply chain normalization, a moderate slowdown in economic activity, and tighter monetary policy. Core Personal Consumption Expenditures (PCE) inflation, which excludes volatile prices such as energy and food, fell to a new low of 2.6% in June, the slowest pace in more than three years. Importantly, shelter inflation, the main component sustaining core inflation, is set to decelerate further in the coming months, as moderating rental prices are gradually incorporated into new contracts. This will help to cover the proverbial “last mile” gap between the running inflation rate and the inflation target, giving the reassurance that the Fed needs to modify its course and start a policy easing cycle.

Second, softening labour markets suggest not only a lack of more structural price pressures from wages, but also even a potential sharp deceleration of economic activity. Major labour related gauges and surveys, such as the Job Openings and Labor Turnover Survey (JOLTS), the ISM Employment Indices and the Small Businesses Survey, point to quickly deteriorating labour conditions. Temporary employment, for example, is contracting, a condition that usually occurs only during economic recessions. The unemployment rate has gone up sharply from 3.4% in April 2023 to 4.1% in June. But high frequency data from the Kansas City Fed suggests that the unemployment rate could approach 5% over the coming months, far surpassing the estimated “balanced full employment” rate of 4%. This would then place the Fed behind the curve in achieving its “full employment” mandate, requiring a more proactive monetary policy easing stance.

Third, the record monetary tightening cycle has left real interest rates at overly restrictive levels. The real interest rate adjusts nominal interest rates by the level of inflation, and therefore reflects the true hurdle rate by taking into account changes in the prices of goods and services. Real interest rates influence consumer spending, savings, and investment decisions, and therefore affect overall economic activity. A nominal policy interest rate of 5.5% currently implies a real rate of interest above 2%. This is significantly above the “neutral rate of interest” for the U.S. economy of 50-100 bps, which is the level of the real rate that neither stimulates nor restrains economic activity. Thus, current real rates are excessively restrictive and need to be adjusted before causing a sharper slowdown of the US economy.

All in all, we expect the Fed to cut rates by 25 bps twice in 2024, before accelerating the pace of rate cuts in H1-2025. This is due to the continuation of the disinflation trend, a rapidly deteriorating labour market, as well as the need to normalize highly restrictive real rates.

Download the PDF version of this weekly commentary in

English

or

عربي