Each summer, the US Federal Reserve (Fed) hosts a highly anticipated economic policy symposium in Jackson Hole, Wyoming. This gathering is among the most established central banking conferences globally, drawing leading economists, bankers, market participants, academics and policy makers to deliberate on long-term macroeconomic challenges.

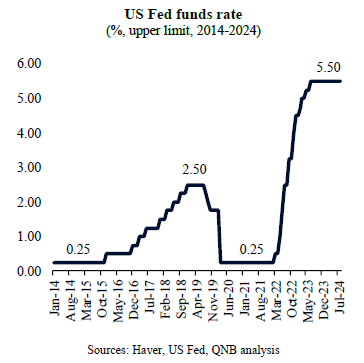

Although the Jackson Hole Symposium consistently holds a significant place on the economic calendar for investors and policy makers, this year, its significance was particularly pronounced. For the first time in half a decade, Jackson Hole took place amid discussions of starting a cycle of meaningful monetary policy easing. This follows one of the most aggressive processes of monetary policy tightening in decades.

Importantly, the symposium took place in a period of speculation about how deep and how fast the Fed will enact its easing pivot. After months of caution and maintaining rates higher for longer on the back of still above target inflation, investors were waiting to observe the tone of Fed officials for the next Federal Open Market Committee (FOMC) meetings. The prevalent view was that US inflation is set to gradually return to target.

Throughout the symposium, the overall tone from Fed officials was decisively “dovish,” i.e., biased towards a more aggressive rate cutting cycle. According to Fed Chairman Jerome Powell, “the upside risks to inflation have diminished and the downside risks to employment have increased.” Moreover, Powell stressed that the direction of policy rates is clear, as the priority of monetary authorities are rapidly shifting from containing inflation to preventing further “labour market erosion and pain.”

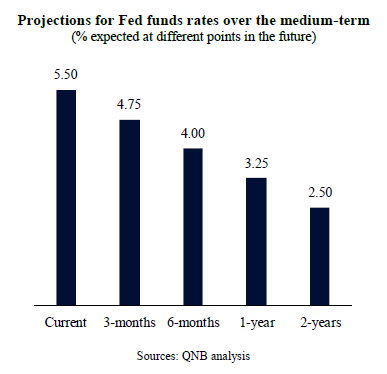

In our view, the Fed will continue to lean “dovish,” cutting rates by an accumulated 75 basis points (bps) this year, before continuing with further cuts in 2025. In fact, we expect the upper limit of the Fed funds rate to be at 3% in late 2025, before bottoming for the cycle at 2.5% in 2026. Two main factors sustain our view.

First, while headline Consumer Price Index (CPI) inflation is still 90 bps above the 2% target, forward-looking indicators point to strong disinflationary trends ahead. If we exclude shelter inflation, tracking housing costs and rent as the largest CPI component, the inflation rate is even below the 2% target. This suggests that inflation has been successfully controlled and that the time has come for the Fed to adjust interest rates and monetary policy.

Second, the labour market has already adjusted significantly, with the unemployment rate increasing from 3.4% to 4.3% since January 2023, reaching the upper range limit of what the Fed considers “full employment.” This has been sufficient to tame wage pressures to a level that is aligned with a 2% inflation target. However, there is a risk that negative job market trends gain further momentum, leading to unemployment levels and undue deflationary pressures.

Third, as both inflation and real GDP growth slowdown rapidly in the US, the effective monetary policy stance tightens, increasing the burden of higher rates on households and corporates. Hence, in order not to be left too much “behind the curve,” i.e., with an inappropriate policy rate, the Fed needs to act firmly. The outlook suggests a neutral rate of 3%. Hence, in order to prevent a sharper slowdown and deliver the expected “soft landing,” the Fed is likely going to have to enter accommodative territory with below 3% policy rates.

All in all, conditions are in place for the Fed to start a significant easing cycle. Inflation is effectively on target, “full employment” is at risk and overall macro conditions are aligned for a battery of policy rate cuts.

Download the PDF version of this weekly commentary in

English

or

عربي