Every summer, the European Central Bank (ECB) organizes a sought-after monetary policy forum in Sintra, Portugal. The event is one of the most important central banking conferences in the world, bringing together top economists, bankers, market participants, academics and policy makers to discuss relevant macro issues.

Since its inception in 2015, the forum has garnered significant attention due to the impactful speeches delivered by senior policymakers, rivalling the Jackson Hole conference in its appeal to investors.

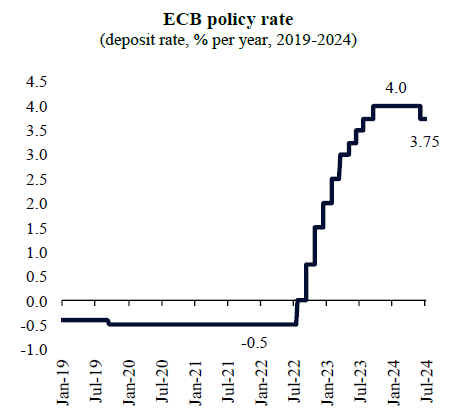

As an ECB-led event, it has always held prominence on investors’ calendars. Indeed, this year’s meeting was particularly relevant, as the ECB had just started a new phase of its monetary policy cycle last month, when policy rates were cut for the first time in five years. This came after a “holding” period of nine months, which followed the most aggressive tightening in the history of the ECB, when rates were hiked by 425 basis points (bps) as a response to the post-pandemic inflationary shock.

However, despite the beginning of the easing cycle, there is still significant uncertainty about the pace of rate cuts going further, as well as the “terminal rate” or “neutral rate” at which the nominal policy rate should stabilize.

In the introductory speech of the Sintra forum, Christine Lagarde, the president of the ECB, expressed well what is behind the hesitation to take a more aggressive path towards a faster monetary policy easing: “Now, we are still facing several uncertainties regarding future inflation, especially in terms of how the nexus of profits, wages and productivity will evolve and whether the economy will be hit by new supply-side shocks. And it will take time for us to gather sufficient data to be certain that the risks of above-target inflation have passed.”

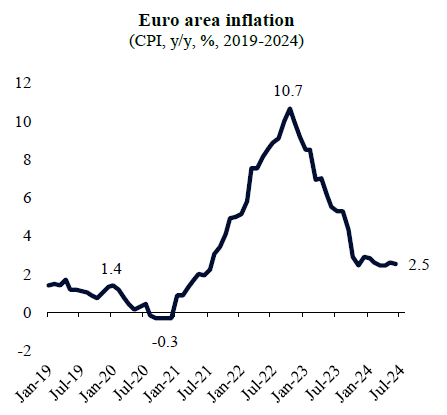

With inflation still running at 2.5% y/y in June, above the 2% target of the ECB but much below the recent peak from October 2022, there is comfort for the beginning of an easing cycle but still no consensus for a more “dovish” stance, i.e., faster rate cuts.

In our view, insights shared during the meeting by senior ECB officials pointed to a rather unusual economic cycle, which increases uncertainty and requires a more nimble, data dependent approach to monetary policy.

Despite five straight quarters of stagnation since late 2022, the Euro area economy has so far avoided a sharper downturn. This is an unusual outcome given the magnitude of the supply shocks that had to be tamed, such as the Covid pandemic and the Russo-Ukrainian War. These events had major implications, such as input shortages, a regional energy crisis and the de-anchoring of fiscal policies, which caused wider budger deficits and higher government indebtedness. The ECB had to then respond strongly, taking policy rates to restrictive levels in order to re-anchor inflation expectations.

In previous periods, such negative headwinds from external shocks and central bank policy would have produced a more pronounced recession. This time, however, seems to be different. A mix of labour shortages, fiscal expansion and nominal earnings growth contributed to support exceptionally benign labour markets, despite the stagnant economy. In fact, the unemployment rate is at all-time lows at the same time that wages are still growing at more than 4% per year. The lack of more severe weakness in labour markets prevents the ECB from embarking on a firmer policy easing stance.

According to Christine Lagarde, “the strong labour market means that we can take time to gather new information, but we also need to be mindful of the fact that the growth outlook remains uncertain. All of this underpins our determination to be data dependent and to take policy decisions meeting by meeting.”

All in all, we expect to see the ECB enact two more 25 bps rate cuts this year, as it continues to closely monitor the evolution of prices and labour market activity.

Download the PDF version of this weekly commentary in

English

or

عربي