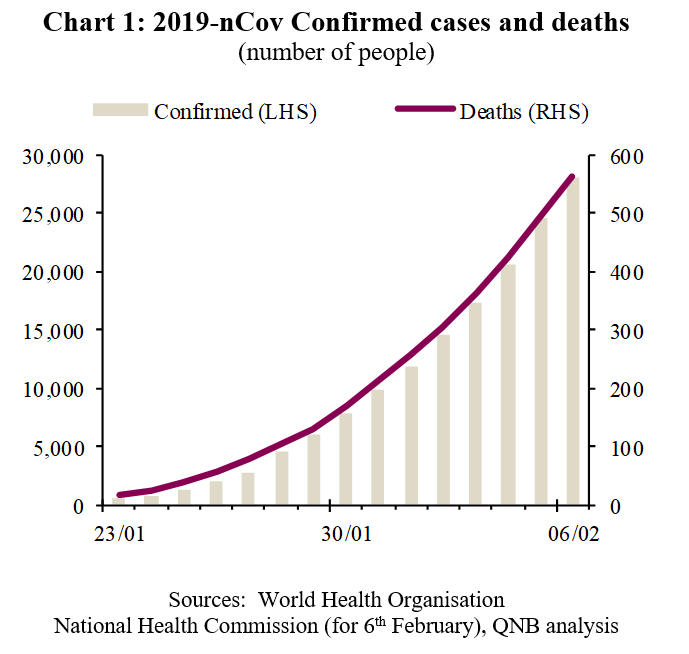

In December 2019 the Chinese authorities detected a novel coronavirus in Wuhan City, Hubei Province. The virus, now known as 2019-nCov, has already infected over 28,000 and killed more than 560 people (Chart 1). Our sympathies to all those who have been affected.

Last week we highlighted the likely drag on economic growth in emerging Asia, primarily via a hit to tourism. However, the virus is spreading quickly and the number of newly confirmed cases is continuing to rise, particularly in China. Therefore, this week we take a closer look at the virus and focus on quantifying the direct impact of weaker Chinese GDP growth on global GDP growth.

SARS was more deadly but less infectious

The Severe Acute Respiratory Syndrome (SARS) outbreak in 2002-2003 infected nearly 9,000 people in 17 countries and killed around 10% of those infected. In comparison, 2019-nCoV has already infected more people than SARS, but appears to have a much lower mortality rate, only killing 2-3% of those infected so far. Normal seasonal flu is another relevant comparison. 2017/18 was a bad flu season in the USA with 45 million people displaying symptoms but only 61,000 flu-related deaths, which is only 0.14% of those infected.

Aggressive measures taken to contain the virus

In response to the increasing severity of the outbreak, authorities in China have implement travel bans, quarantines, and closures of factories and leisure facilities. The decision to quarantine the whole of Wuhan City from the 23rd January is important because 2019-nCov has an incubation period of up to 14 days and it will take this long for us to start to see a reduction in the rate of newly confirmed cases.

Travel restrictions led to a fall in passengers within China during the Lunar New Year holiday of up to 50% across road, rail and air transport. Factory and business shutdowns have been imposed on 14 provinces and cities across China, including the main industrial centre. Together, they account for 70% of China’s GDP and 80% of exports. With the virus continuing to spread, it is likely the shutdowns will be extended beyond the 10th February.

Automotive and energy demand will be hit

Chinese automotive sales are set to fall by 25% to 30% in the first two months of 2020, with the virus likely to drag down China’s full-year auto sales by as much as 5%. Likewise, Chinese car production is forecast to fall by 15% during Q1.

China is the world largest importer of crude oil and second largest importer of LNG. Oil imports are estimated to have fallen by 25% already, which will reduce fuel production by refineries and delay crude shipments. Similarly, lower gas demand is prompting Chinese gas buyers to consider reducing import volumes, given already high inventories.

2020 Chinese GDP growth will now be weaker

It is worth noting that it is the measures to contain the virus, particularly the travel bans and extended factory shutdowns, that are causing almost all of the economic damage rather than the virus itself.

We expect Chinese GDP to be 2 percentage points (ppt) weaker in Q1 2020, down to 4% year-on-year from 6% in Q4 2019. But a recovery from Q2 onwards would limit the impact on full-year GDP growth to less than 1 ppt. The full-year impact could easily be twice as large in a more severe scenario if travel restrictions and shutdowns extend into Q2.

China is now large enough to impact Global GDP

China now accounts for around 20% of the global economy at purchasing power parity (PPP) exchange rates. Therefore, a 1 ppt fall in Chinese GDP growth (our base case) would knock 0.2 ppt off of the IMF’s projection of 3.3% global GDP growth in 2020. Further, our more severe scenario would knock 0.4 ppt off of global GDP, lowering it to only 2.9% in 2020 and wiping out all of the expected pick-up in growth from 2.9% in 2019.

Those simple calculations ignore the indirect negative impact on GDP in other countries via tourism, supply chain disruption, and weaker Chinese demand for commodities. However, they also ignore the positive impact on GDP from policy stimulus (both fiscal and monetary) China and other countries. We expect these impacts to offset each other, making the simple calculations a good starting point for assessing the potential impact.

Conclusion

The severity of the outbreak of nCov-2019 has increased with the number of confirmed cases of infection. Likewise, the likely economic impact has become more significant with the extension of measures take to contain the virus. We do not yet know whether it will take weeks or months to bring the virus under control. However, the simple scenarios and calculations presented here tell us that nCov-2019 may have already halved the pick-up in global growth in 2020 and there could be no pick up.

Download the PDF version of this weekly commentary in English or عربي